Against the Tide

Asset Class Returns for 2023

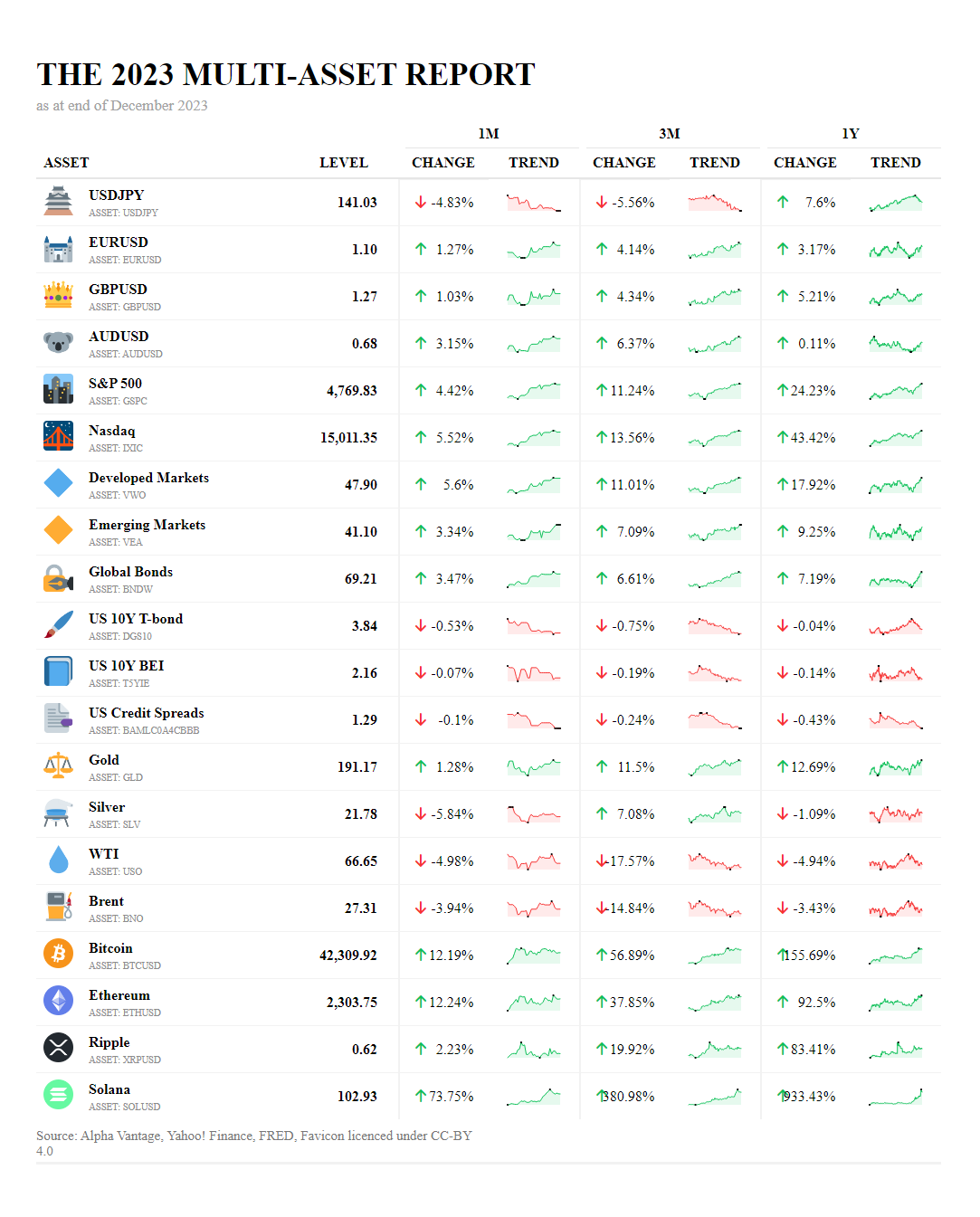

2023 is a year that has been dominated by global geopolitical turmoil, monetary policy, with a looming recession in parts of the global economy creating an undercurrent of unease. Yet, in this seemingly challenging economic landscape, risk assets have remarkably outperformed, painting a picture of resilience and investor defiance against the broader backdrop of concern.

* US 10Y T-Bond represents the change in yield no the return of the asset class

** US 10Y BEI reflects the change in the Breakeven Inflation rate not the returns of the asset class

*** US Credit Spreads represents the change in the spread not the not returns of the asset class

In the currency markets, we've seen the Japanese Yen weaken significantly against the dollar, with the USD/JPY pair up by 7.66% over the year, which reflects the differing monetary policies between the U.S. Federal Reserve's rate hikes and the Bank of Japan's continued dovish stance. We have seen this dynamic reverse in recent months as the Fed paused its trajectory of The Euro and British Pound have shown modest gains against the dollar, suggesting that investors may be finding value in these currencies as potential hedges against dollar strength and inflation.

Equities have surged forward, with the S&P 500 and Nasdaq posting annual gains of 24.23% and 43.42%, respectively. This robust performance indicates that investors are channeling funds into growth-oriented sectors, betting on the resilience of corporate earnings and technological innovation, especially in AI to counteract inflationary pressures.

Interestingly, Developed Markets and Emerging Markets equities have also performed well, with annual returns of 17.92% and 9.25% respectively. This could point towards a divergence in economic recovery paths or an appetite for risk-taking even in less stable regions.

In the bond market, the relatively stable US 10-Year Breakeven Inflation rate implies that inflation expectations have been somewhat anchored, despite the actual inflationary pressures. Meanwhile, US credit spreads have contracted slightly, suggesting that credit risk has not escalated to the extent that might be expected in a typical pre-recession environment.

Gold has traditionally been a haven in times of inflation, and with an annual increase of 12.69%, it seems to fulfill this role once again. However, Silver has not fared as well, declining by 1.09% over the year, which could be due to its dual role as both an investment and an industrial metal.

In the energy sector, despite volatilities caused by geopolitical turmoil in oil sensitive region, both WTI and Brent crude have seen annual declines, which could be a response to fears of reduced demand in a slowing economy and also an increase in uptake of alternative energy sources.

The cryptocurrency market, on the other hand, has seen an explosive increase with Bitcoin and Ethereum rising by 155.69% and 92.5% over the year, respectively. This extraordinary performance, particularly in the context of economic uncertainty, underscores the growing acceptance of cryptocurrencies as a legitimate asset class and a potential hedge against inflation.

In summary, the multi-asset performance of 2023 can be characterized as one of dichotomy. With traditional safe-haven assets and risk assets both advancing, it reflects a market that is hedging its bets—balancing the potential for growth against the ongoing economic uncertainty. Investors have navigated this complex landscape with a clear tilt towards growth and innovation, while remaining cognizant of the value of diversification in a period marked by significant macroeconomic challenges.

"It's not whether you're right or wrong that's important, but how much money you make when you're right and how much you lose when you're wrong." - George Soros