Backoff

End of Week Markets Breakdown 05/06/2026

Overview

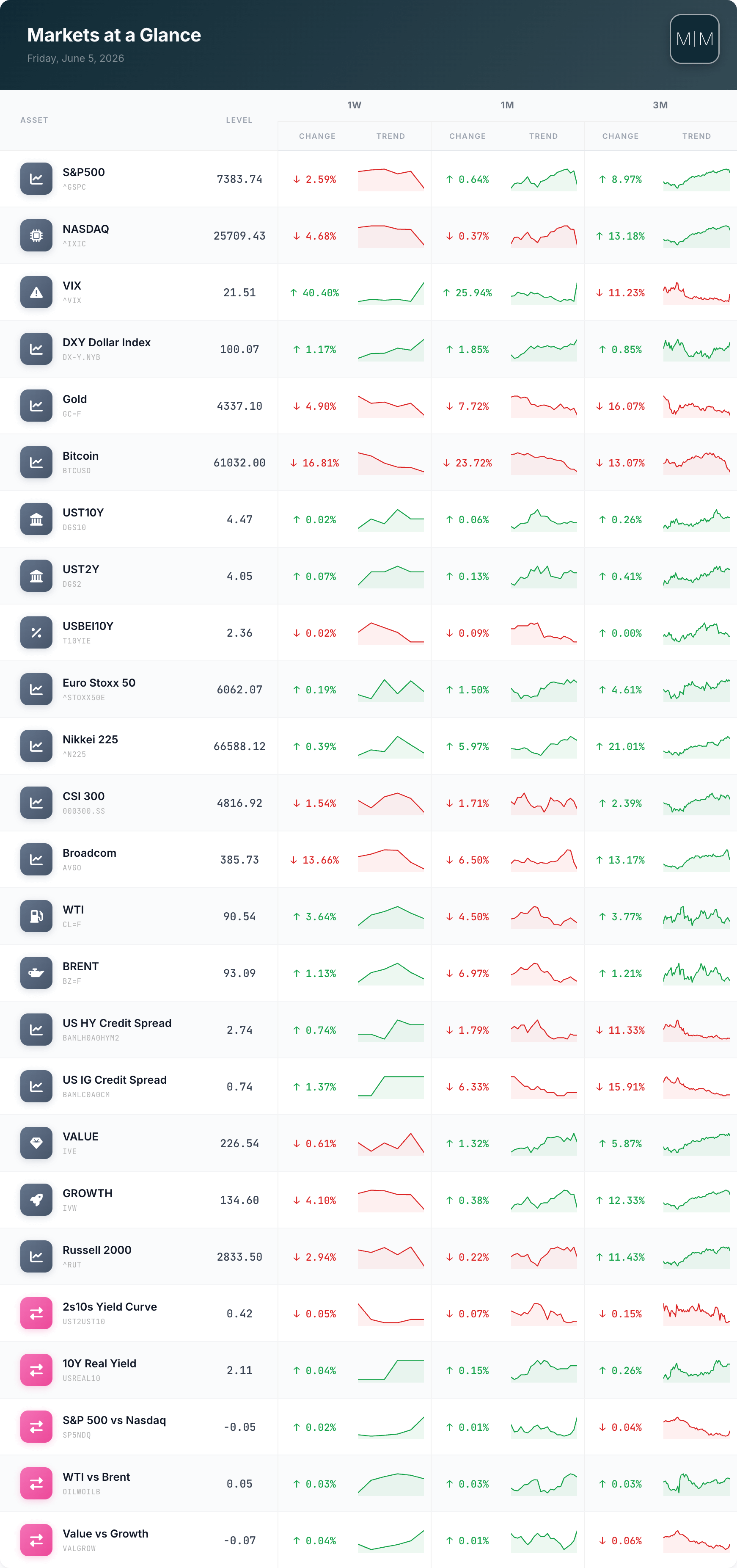

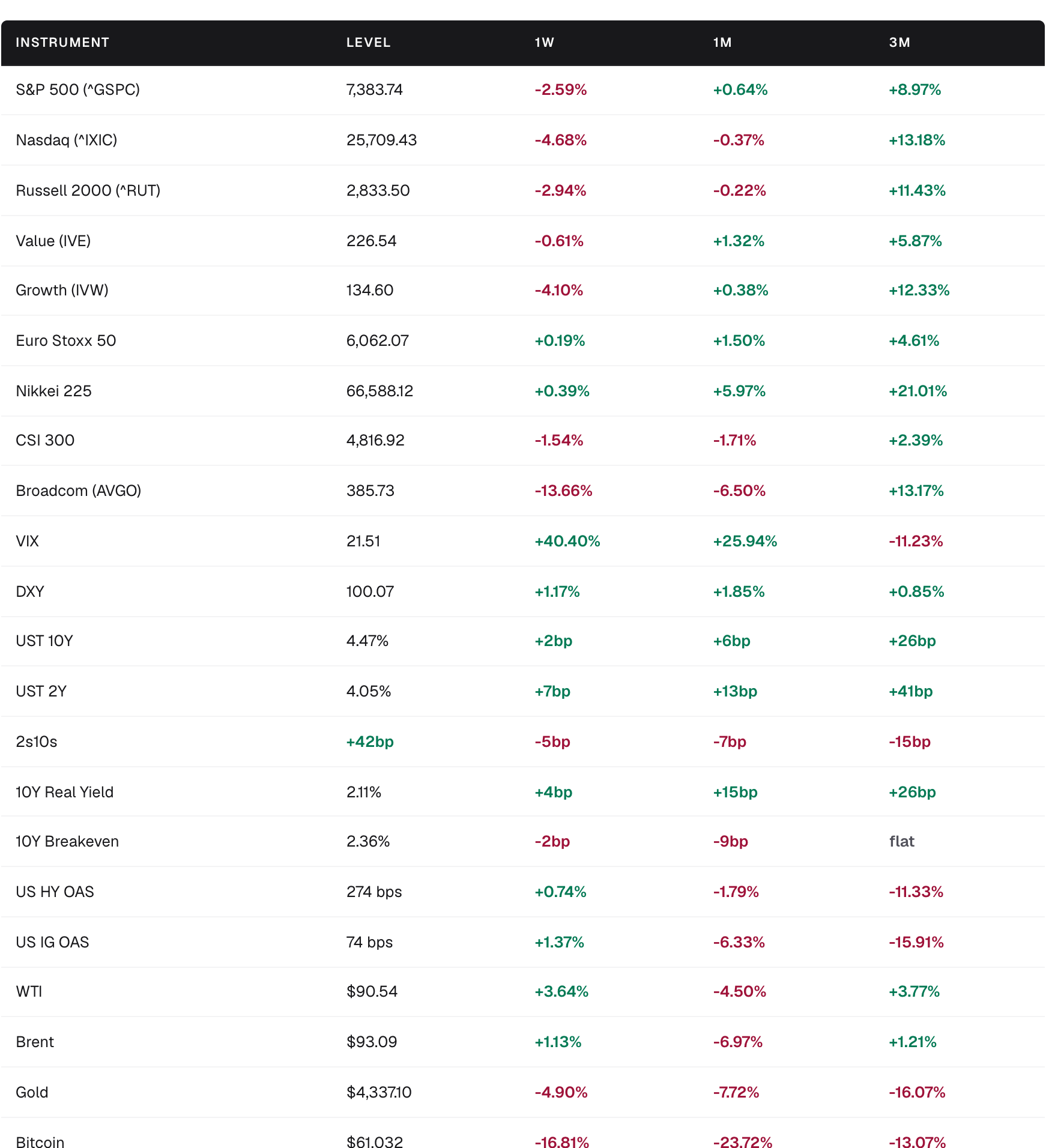

Risk assets cracked after a long grind higher: the S&P 500 fell 2.59% on the week to 7,383.74 and the Nasdaq dropped 4.68% to 25,709.43, with the latter posting its worst session since April 2025 mid-week.

Volatility woke up sharply: the VIX surged 40.40% on the week to 21.51, while the DXY firmed 1.17% to 100.07 as cash and dollars caught a bid.

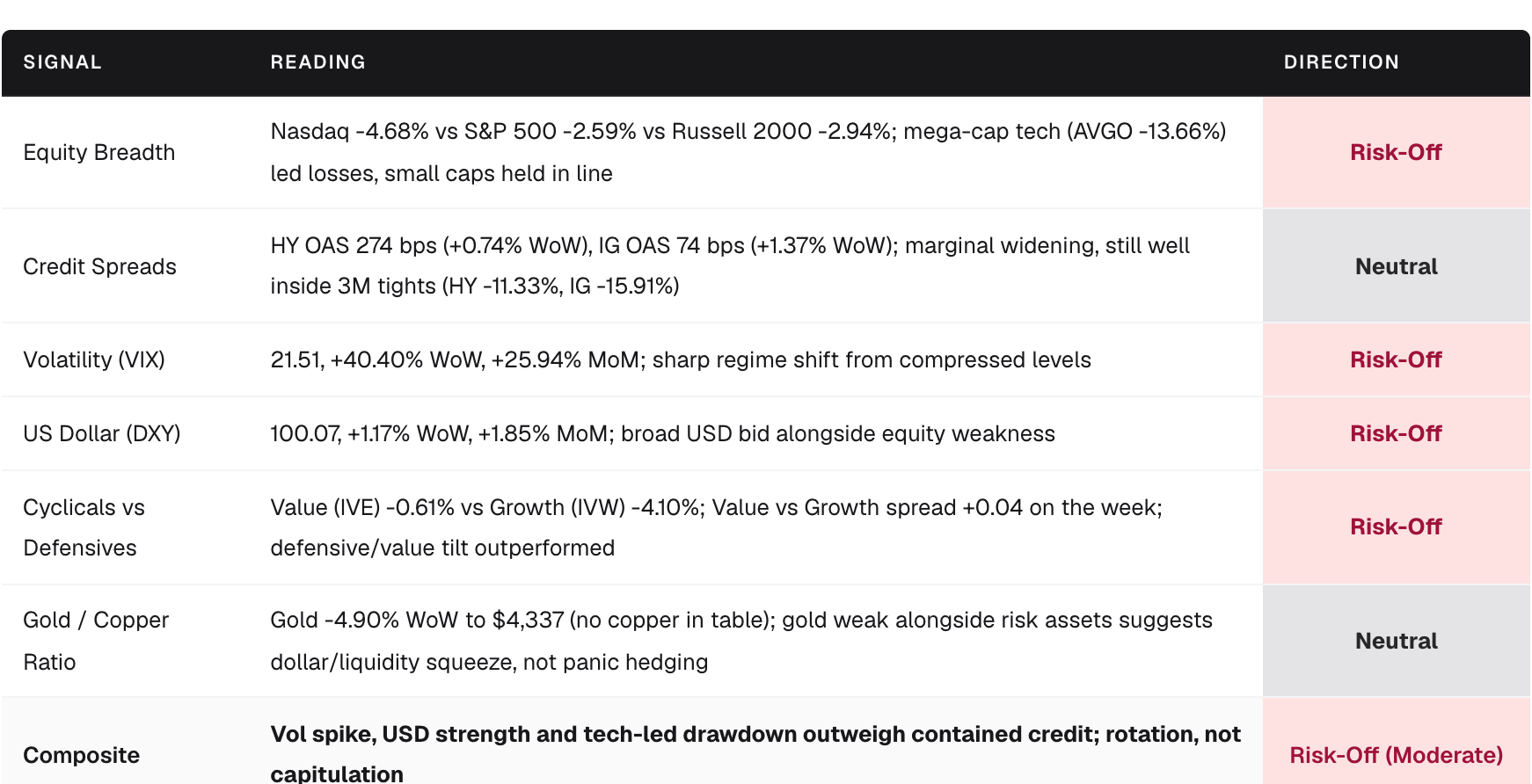

The sell-off looked like a rotation, not a credit event: HY OAS was only marginally wider (274 bps, +0.74% WoW) and IG OAS 74 bps (+1.37%), value (IVE) fell just 0.61% versus growth (IVW) down 4.10%.

Crypto and gold both broke down hard: Bitcoin slumped 16.81% to $61,032 and gold fell 4.90% to $4,337, an unusual joint de-risking that points to forced deleveraging and a stronger dollar rather than classic flight-to-safety.

Geopolitics (Iran/Strait of Hormuz) lifted oil (WTI +3.64% to $90.54) while Treasuries barely moved (10Y at 4.47%, +2bp), leaving real yields (2.11%, +4bp) as a quiet headwind to long-duration tech.

Market Scorecard

Market Performance

A week dominated by a U.S. tech-led drawdown. Europe was nearly flat (Euro Stoxx 50 +0.19%) and Japan eked out a gain (Nikkei +0.39%), highlighting concentrated pressure on U.S. growth/AI names rather than a global growth scare. Rates were essentially unchanged, with the 2s10s curve flattening 5bp to +42bp. Oil firmed on Gulf tensions while gold and bitcoin both sold off alongside equities, an unusual correlation pattern consistent with a dollar/liquidity squeeze.

Key Drivers

AI/semis derating: Broadcom’s fiscal Q2 print reaffirmed AI demand, but the stock fell 13.66% on the week, suggesting positioning, not fundamentals, drove the unwind in AI infrastructure names.

Geopolitics, Iran conflict: continued US-Israel-Iran tensions and Strait of Hormuz shipping risk kept a bid under oil (WTI +3.64%), but markets continued to treat the conflict as tail risk, not base case.

Real yields grinding higher: 10Y real yield at 2.11% (+4bp WoW, +26bp over 3M) is a quiet headwind for long-duration growth multiples, even as nominal 10Y barely budged.

Data-light week, pre-CPI positioning: no top-tier US, Euro area, UK, Japan or China prints in the window; flows were dominated by de-risking ahead of the 10 to 12 June CPI/PPI/UoM gauntlet.

Fed research note (2 June) on bank equities and geopolitical risk formalized geopolitical risk as a systemic monitoring channel, but no new policy action from the Fed, ECB, BoE, BoJ or PBoC was reported in the window.

Dollar resurgence: DXY +1.17% to 100.07 amplified pressure on gold, bitcoin, and EM-linked risk.

Sector and Thematic Notes

AI infrastructure / mega-cap tech: clear loser. AVGO -13.66%; Nasdaq -4.68% vs S&P -2.59% confirms concentration in growth pain. Narrative intact, positioning the issue.

Value vs Growth: value held up materially better (IVE -0.61% vs IVW -4.10%); the VALGROW spread improved +0.04 on the week, reversing a portion of the 3M growth lead.

Energy: relative winner. WTI +3.64% and Brent +1.13% on Gulf risk premium; one of the few risk assets up on the week.

Consumer: research flagged Dollar General and Lululemon results pointing to a softer low-end US consumer with resilient international demand; no index-level shock, but a watch item for staples/discretionary dispersion.

Crypto: Bitcoin -16.81% led alternative-asset capitulation; with gold also down 4.90%, the move reads as deleveraging and dollar strength rather than a rotation into safe havens.

Japan vs China: Nikkei +0.39% (+21.01% on 3M) continued to outperform CSI 300 (-1.54% WoW), reinforcing the regional bifurcation theme.

Credit: IG and HY both modestly wider but well behaved; spreads not validating the equity vol spike, which historically argues against extending the drawdown unless credit confirms.

Risks to Watch

May US CPI/PPI (10 to 11 June): a hot print into a now-fragile tape could push real yields higher and extend the growth derate; a soft print is the most obvious mean-reversion catalyst.

Credit confirmation: HY OAS at 274 bps is still near cycle tights; a decisive break wider would shift the read from “rotation” to “risk event.”

Strait of Hormuz escalation: any tangible disruption to Gulf energy flows would re-rate oil and reintroduce a stagflationary impulse the curve is not pricing.

Volatility regime change: VIX +40% off compressed levels often presages a period of elevated realized vol; systematic strategies (vol-target, CTA) could amplify de-risking flows.

Dollar squeeze: DXY back to 100 with bitcoin and gold both down is a tell for tightening dollar liquidity; sustained USD strength would pressure EM, commodities, and US multinational earnings.

Positioning Implications

Rebalancing rather than capitulating: with credit contained and breadth losses concentrated in growth, this week looks more like a positioning flush than a regime change. Consider trimming, not abandoning, AI/growth concentration.

Style barbell: the value/growth dispersion (IVE -0.61% vs IVW -4.10%) argues for keeping some defensive/value ballast alongside secular growth exposure rather than running a pure-growth book into the CPI print.

Duration as a hedge has been weak: 10Y unchanged through a 40% VIX spike confirms the bond hedge is less reliable while real yields drift up. Consider quality credit and short-duration carry alongside, or in place of, long-duration Treasuries.

Energy as a geopolitical hedge: long energy continues to function as the cleanest expression of Middle East tail risk while offering positive carry.

Dollar exposure: with DXY breaking back to 100, unhedged non-USD positions warrant a review; the move has already pressured gold and crypto.

Volatility: outright vol is no longer cheap (VIX 21.5), but skew, dispersion, and downside puts on concentrated AI names remain reasonable expressions if hedging into the CPI window.

Crypto and gold: the joint drawdown highlights that “alternative store of value” allocations can correlate to one in dollar-liquidity events; size accordingly.

Cross Asset Performance Report