Bottleneck

End of Week Breakdown - 26/04/2026

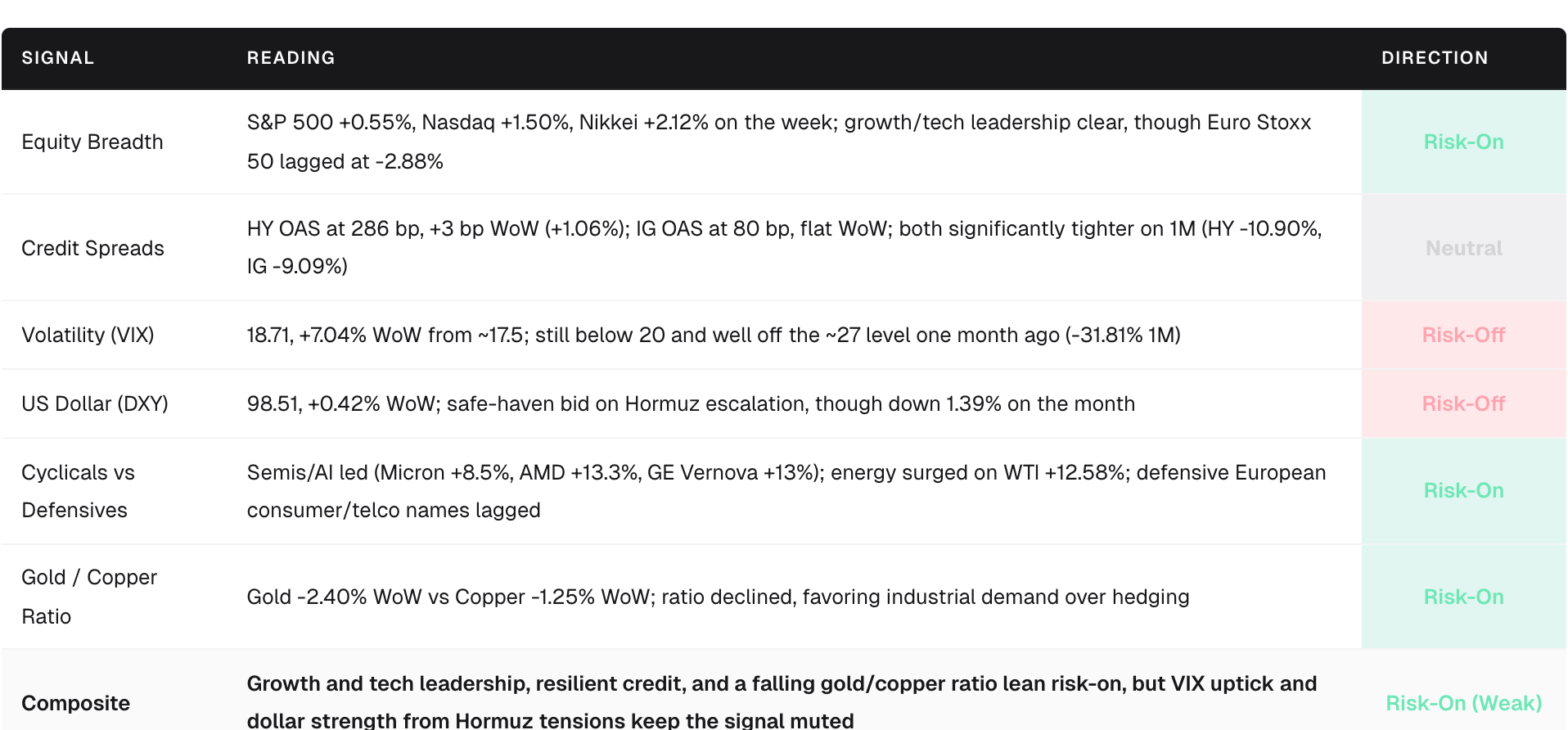

Overview

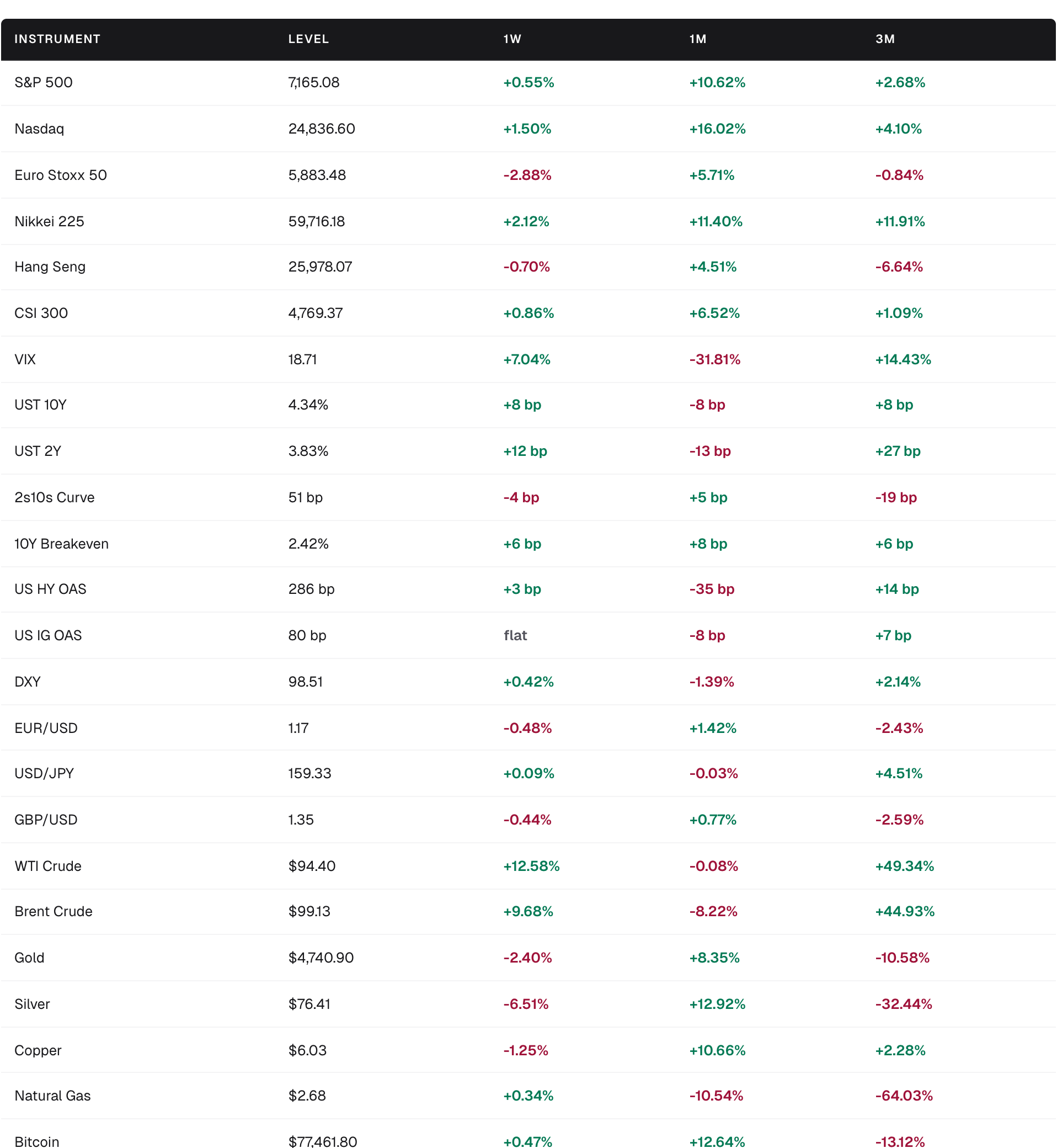

US equities eked out gains despite late-week geopolitical turbulence: the S&P 500 rose 0.55% to 7,165 and the Nasdaq climbed 1.50% to 24,837, buoyed by tech/AI earnings strength. Mid-week records were tested on US-Iran ceasefire optimism, then trimmed as Strait of Hormuz tensions re-escalated.

Oil was the dominant story. WTI surged 12.58% to $94.40 and Brent jumped 9.68% to $99.13 on Hormuz disruption fears, an Iranian ship seizure, and closure threats. The energy shock lifted 10Y breakeven inflation by 6 bp to 2.42%.

Central banks enter a holding pattern. The Fed (April 29), ECB and BoE (April 30), and BoJ (April 27 to 28) are all expected to hold rates steady; messaging around inflation persistence and energy-driven price pressures will be the key variable.

European equities sharply underperformed (Euro Stoxx 50 down 2.88%), reflecting industrial and consumer exposure to rising energy costs. Japan outperformed (+2.12%) on semiconductor and AI tailwinds.

Precious metals sold off (gold down 2.40%, silver down 6.51%) despite geopolitical uncertainty, as a firmer dollar (+0.42%) and modestly higher real yields (+2 bp) redirected flows away from non-yielding assets.

Market Scorecard

Market Performance

Key Drivers

Strait of Hormuz escalation. Iran fired on ships, threatened closure, and the US seized an Iran-linked vessel, puncturing a brief ceasefire extension. WTI spiked 12.58% in a single week, the largest weekly gain in over a year, pushing Brent to within a dollar of $100.

Breakeven inflation repricing. The energy shock lifted 10Y breakevens by 6 bp to 2.42%, complicating the path for rate cuts and shifting attention to PCE data due April 30.

US-Iran ceasefire dynamics. President Trump extended an indefinite ceasefire mid-week, triggering a brief risk-on session (S&P +1.1% on April 23). Tehran’s subsequent rejection of peace talks reversed sentiment.

Semiconductor/AI earnings strength. Intel reported strong results, lifting AMD (+13.3%), Micron (+8.5%), and ASM International (+7.1%). GE Vernova surged 13% on a raised 2026 outlook tied to data-center power demand.

Central bank pre-positioning. Markets priced no change across the Fed (3.50% to 3.75%), ECB, BoE (3.75%), and BoJ (0.75%), with focus squarely on forward guidance language.

European energy vulnerability. Oil near $100 weighed disproportionately on Euro Stoxx 50 (-2.88%), with DAX and CAC 40 lagging on industrial energy cost exposure, while FTSE 100 showed relative resilience.

Sector and Thematic Notes

Winners:

Energy producers: the week’s standout beneficiaries as WTI rose 12.58% and Brent 9.68%; upstream names rallied on supply fears.

Semiconductors and AI infrastructure: Micron +8.5% (AI chip demand), AMD +13.3%, ASM International +7.1% (strong Q2 guide), SoftBank +8.5% (AI enthusiasm). Nasdaq’s 1.50% weekly gain, triple the S&P’s, underscores the leadership.

Data center power: GE Vernova +13% on raised 2026 outlook driven by data-center buildout.

Japanese equities: Nikkei +2.12% on the week, +11.91% over three months, benefiting from a weak yen (USD/JPY at 159.33), AI/chip demand, and domestic reflation.

Boeing: +5.5% on a smaller-than-expected loss; defense adjacency provided a tailwind.

Losers:

European consumer/telecom: Deutsche Telekom -4.8% (T-Mobile US merger speculation), Reckitt -4.6% (weak results); Euro Stoxx 50 -2.88%.

Precious metals: Gold -2.40%, silver -6.51% on the week. Silver down 32.44% over three months, reflecting the collapse in the silver/gold ratio.

Aviation and transportation: pressured by the energy cost surge.

Natural gas: down 10.54% on the month and 64.03% over three months; demand weakness and supply normalization continue.

Hang Seng: -0.70% on the week, -6.64% over three months, lagging global peers on property sector drag and geopolitical overhang.

Risks to Watch

1. Strait of Hormuz closure or further escalation. Brent at $99.13 is one headline away from triple digits. A sustained move above $100 would amplify the inflation impulse, tighten financial conditions, and force a hawkish recalibration by central banks. WTI's +49.34% three-month surge already embeds significant premium; any diplomatic resolution could trigger a sharp unwind.

2. Earnings Superweek concentration risk. Microsoft, Meta, Alphabet, Amazon, and Apple report in the coming days. With Nasdaq up 16.02% on the month and leadership extremely narrow in AI/semis, any guidance miss could catalyze a sharp rotation or broader de-risking.

3. Macro data gauntlet (April 29 to 30). Q1 GDP advance (consensus 2.1%), March PCE core (0.3% MoM expected), ISM manufacturing PMI, and Eurozone flash CPI (2.9% YoY expected) all release within 48 hours. A hot PCE or soft GDP print would sharpen the stagflation debate and pressure both ends of the curve.

4. Central bank messaging surprise. With four major central banks deciding in the span of three days, the risk of a hawkish tilt, particularly from the ECB in response to energy-driven inflation, could catch markets positioned for extended pauses.

5. Dollar feedback loop. DXY at 98.51 is up 2.14% over three months. Further safe-haven appreciation would tighten global dollar liquidity, pressure EM assets (Hang Seng already -6.64% 3M), and weigh on US multinationals' earnings translations ahead of Q2 guidance.

Positioning Implications

Energy: tactically constructive, structurally cautious. The Hormuz risk premium is real but binary. Oil longs have worked (WTI +49.34% 3M), and positioning is likely crowded. Consider expressing the view through energy equities with operational leverage rather than outright crude, and maintain tight risk parameters given the potential for rapid de-escalation reversals.

US tech/AI: hold quality, manage concentration. Nasdaq’s 1.50% weekly and 16.02% monthly gains reflect genuine earnings momentum (Intel, Micron, GE Vernova), but the upcoming mega-cap earnings deluge is a binary event for the entire market. Trimming marginal positions into the event and reloading on any post-earnings dislocation is a prudent consideration.

Europe: underweight bias warranted. Euro Stoxx 50 down 2.88% on the week and 0.84% over three months; energy cost sensitivity is a structural headwind as long as Brent hovers near $100. Selective exposure to European defense and energy names may outperform the index.

Duration: neutral, with a bias toward staying short the front end. The 2Y rose 12 bp versus 8 bp for the 10Y, flattening the curve. Rising breakevens (+6 bp to 2.42%) and a looming PCE print suggest the front end is more vulnerable to hawkish repricing. Extending duration opportunistically on any post-data sell-off is worth considering if real yields (1.92%) push materially above 2%.

Credit: monitor, do not chase. HY OAS at 286 bp is historically tight even with the +3 bp weekly widening. The monthly tightening (-35 bp) has been substantial; the risk/reward for adding credit beta here is asymmetric to the downside if oil sustains above $100 and margins compress.

Precious metals: patience over conviction. Gold’s pullback to $4,741 alongside a firmer dollar and rising real yields may present an entry point for longer-horizon allocators, but the near-term momentum is negative. Copper’s relative outperformance (only -1.25% vs gold’s -2.40%) suggests the growth narrative is intact; the gold/copper ratio bears watching as a real-time risk barometer.

Japan: constructive. Nikkei at 59,716 is up 11.91% over three months, supported by AI/semiconductor demand, a weaker yen (USD/JPY at 159.33), and the BoJ’s expected hold. The post-BoJ meeting (April 27 to 28) reaction will be important; any hawkish surprise pushing JPY stronger could dent the trade.

Cross Asset Performance Report