Bullish in a Bear's Cave

Equities Returns for 2023

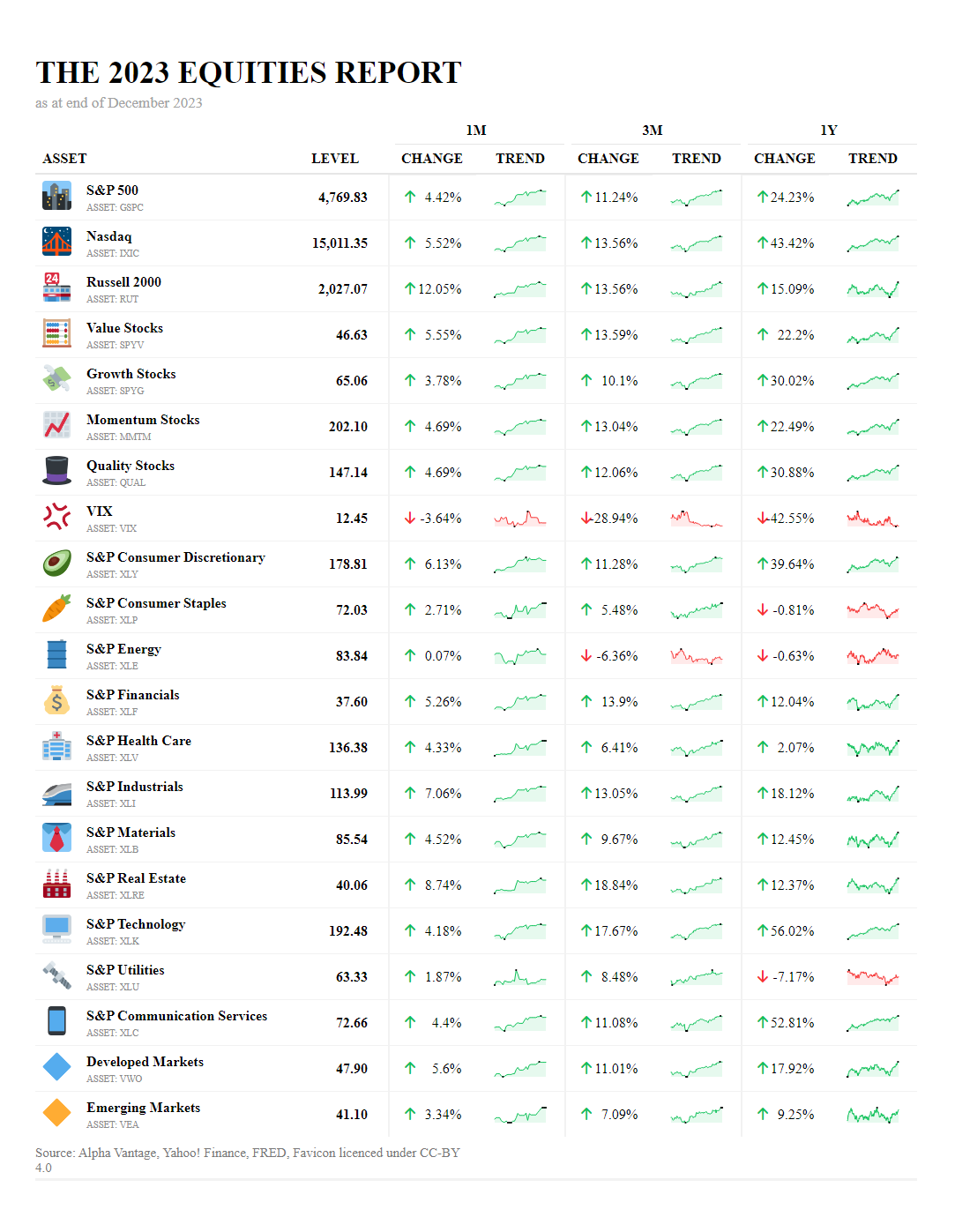

In the face of a macroeconomic landscape dominated by persistent inflation fears and the accompanying rate hikes, the robust performance of the equity markets in 2023 stands in stark contrast. Despite the overhang of a potential recession, equities have managed to deliver substantial returns, a juxtaposition that underscores the complexity of current financial conditions.

The S&P 500 and Nasdaq have posted gains of 24.23% and 43.42% over the year, respectively, suggesting that investors have possibly been looking past short-term economic uncertainties and focusing on the long-term growth potential of large-cap and tech-oriented companies. This bullish sentiment in the face of rate hikes could be attributed to the anticipation of inflation peaking and a subsequent economic recovery.

The Russell 2000's increase of 15.09% indicates that even the smaller companies, which are often more sensitive to economic headwinds, have shown resilience. This could imply that market participants are finding value in more domestically-focused companies, which may be less exposed to global economic turmoil.

While the typical move towards value stocks in inflationary times is visible, with a 22.2% year-on-year increase, the more significant growth in growth stocks at 30.02% suggests that investors are willing to bet on future earnings growth despite the near-term risks. This inclination might reflect confidence in enduring corporate profitability or a scarcity of attractive alternatives.

The reduction in the VIX by 42.55% seems counterintuitive amidst recession fears but may indicate that investors have already priced in the risks and are finding comfort in the market's ability to navigate through these challenging times.

Sector performance has been equally surprising. The Technology and Consumer Discretionary sectors, with annual growth of 56.02% and 39.64%, have thrived even as consumer spending could have been expected to tighten. These sectors' success suggests that innovation and consumer resilience are driving market gains, despite the broader economic headwinds.

Internationally, the resilience seen in Developed and Emerging Markets with annual growth of 17.92% and 9.25% might suggest a divergence in how different economies are managing inflation and interest rate environments, or it could indicate pockets of growth that are less influenced by the US-centric fears of a downturn.

Overall, the performance of the equity markets in 2023 is a testament to the multifaceted nature of investor sentiment and economic outcomes. It suggests a complex interplay of long-term growth expectations countervailing the prevailing narrative of economic pessimism. Nevertheless, investors should remain vigilant, as the current disconnect between market performance and economic indicators could presage increased volatility if the feared recession materializes. Thus, a balanced and well-considered approach to portfolio management continues to be essential.

**special mention to Tanya Shapiro for the excellent reactable template

"The stock market is a device for transferring money from the impatient to the patient." - Warren Buffett