Confidence in the Climb

Equities Report 1

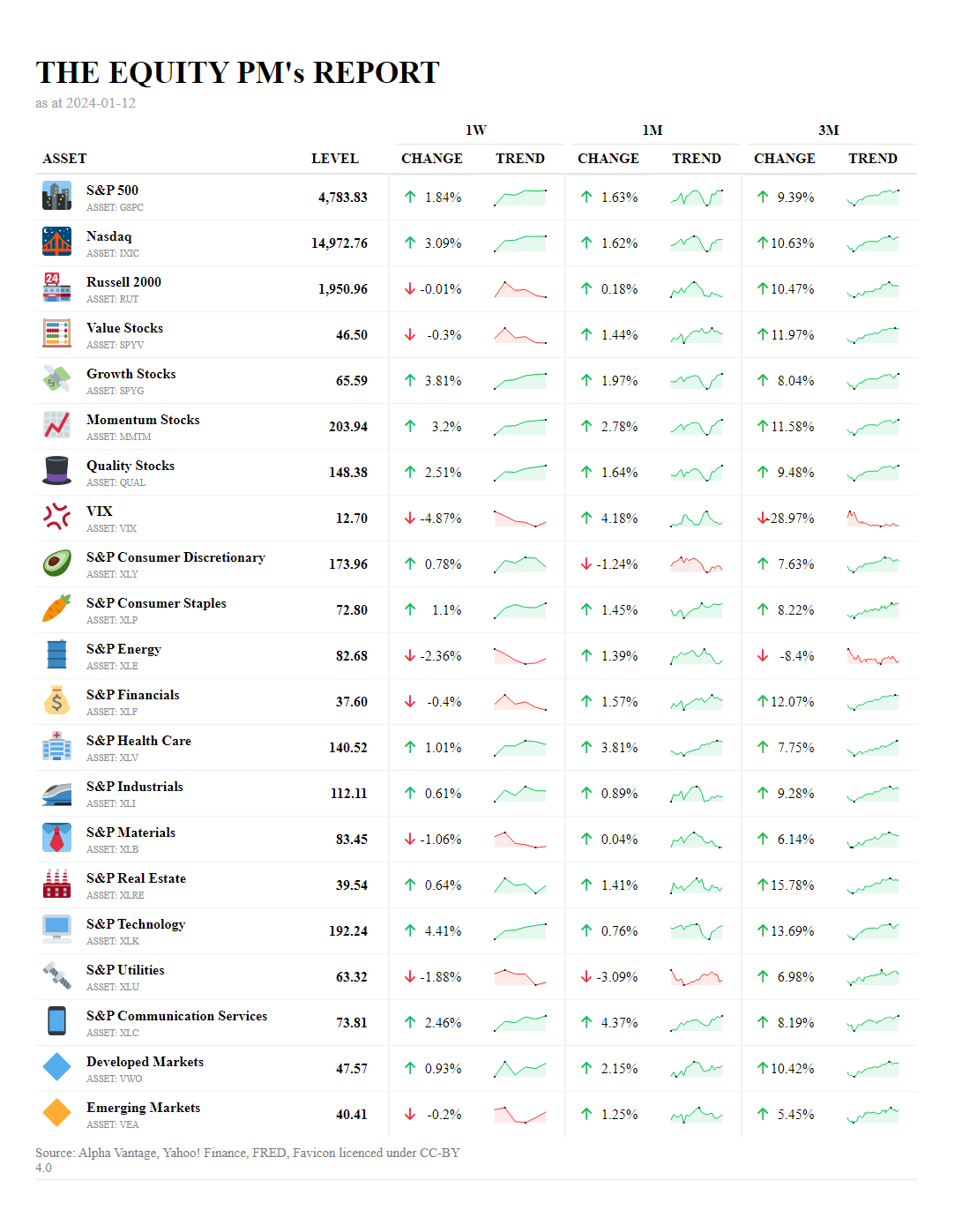

Broad market indices, the S&P 500 and Nasdaq, registered impressive weekly increases of 1.84% and 3.09%, respectively, maintaining their strong upward momentum over one and three months. This solid performance, particularly from the technology-driven Nasdaq, signals a strong investor appetite for risk assets and firm confidence in the innovation sector.

The Russell 2000 index held steady over the past week, taking a breather after a significant three-month gain of 10.47%, which reflects a strategic pause in small-cap investments.

Growth stocks outshone other styles with a remarkable 3.81% rise over the week, extending their dominance over a three-month period with an 8.04% gain. Momentum stocks followed suit, posting a substantial weekly gain of 3.2%, confirming that trend-following strategies are effectively capturing market gains.

Quality stocks, known for their stable earnings and robust balance sheets, surged by 2.51% this week, reinforcing a three-month trend of 9.48%. This underscores the market's preference for financially solid companies amidst current economic conditions.

The VIX plummeted by 4.87% over the week, with a three-month plunge of 28.97%, indicating a market environment characterized by reduced volatility and heightened investor confidence.

Sector analysis shows Technology stocks leading the charge with a significant 4.41% weekly increase, consistent with a bullish three-month trend of 13.69%, which reflects the market's enthusiasm for technological growth and digital transformation.

Conversely, Utilities experienced a downturn of 1.88% this week, despite a positive three-month trajectory, signaling a realignment of investments within the sector.

Health Care and Communication Services sectors also posted strong performances with weekly gains of 1.01% and 2.46%, respectively, driven by a combination of defensive positioning and anticipation of future growth.

The report presents a distinction between Developed and Emerging Markets, with Developed Markets gaining 0.93% over the week, whereas Emerging Markets saw a marginal decline of 0.2%. This indicates a decisive preference for the stability of developed markets amidst global economic fluctuations.

In conclusion, the equities market as of mid-January 2024 is marked

by definite investor confidence, with a pronounced interest in growth-oriented sectors such as Technology and Health Care. Quality and momentum stocks are capturing investor interest, reflecting a strategic approach to capitalizing on market opportunities. The sustained performance of the broader indices and the drop in the VIX point to a market that is not just optimistic but also becoming increasingly secure in its outlook. The slight shift away from Utilities suggests a recalibration towards more dynamic sectors, while the global market's preference leans towards the reliable performance of Developed Markets over Emerging Markets.

"If you have trouble imagining a 20% loss in the stock market, you shouldn't be in stocks." Jack Bogle