Friction

End of Week Markets Breakdown - 22/05/2026

Overview

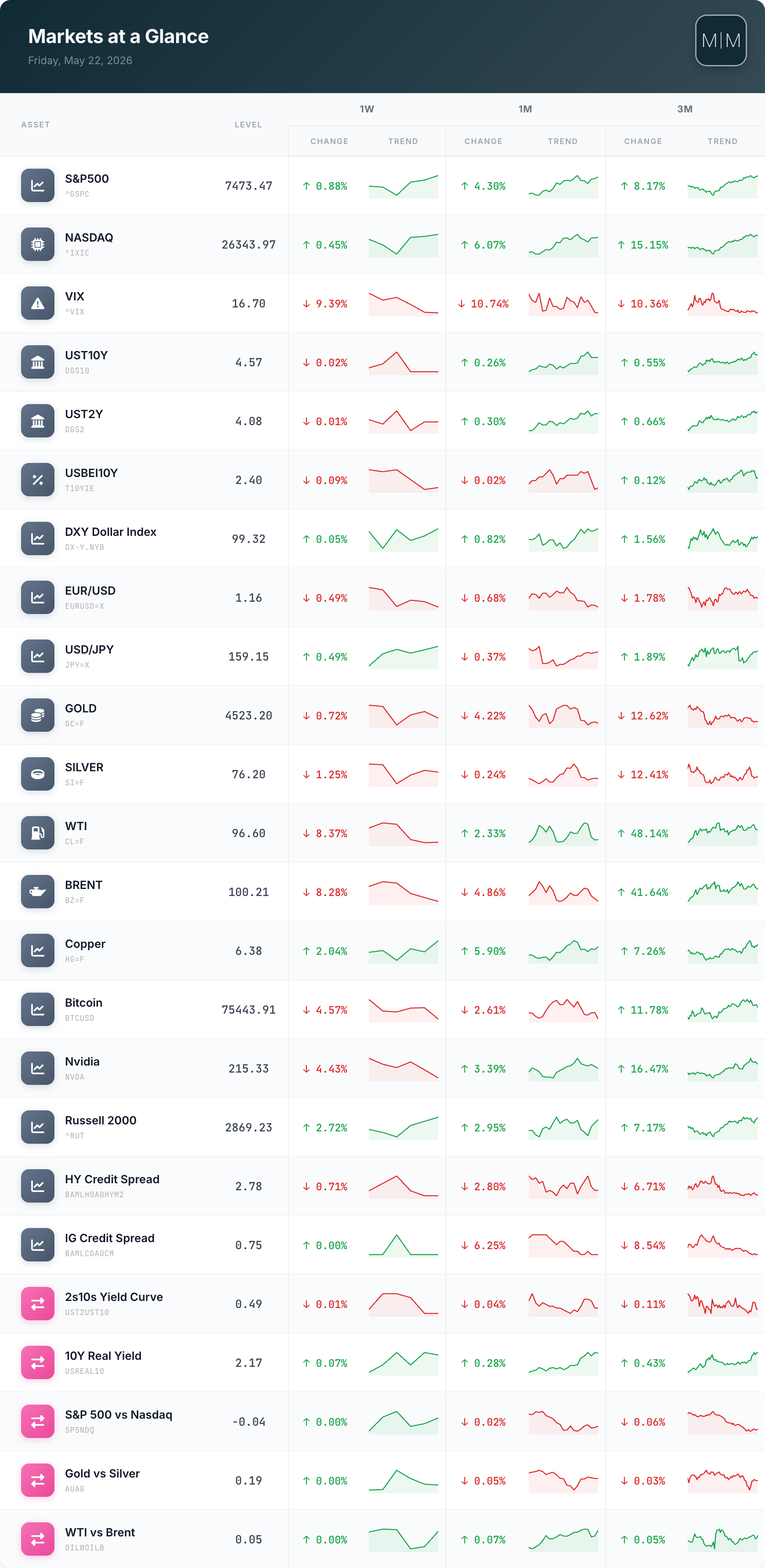

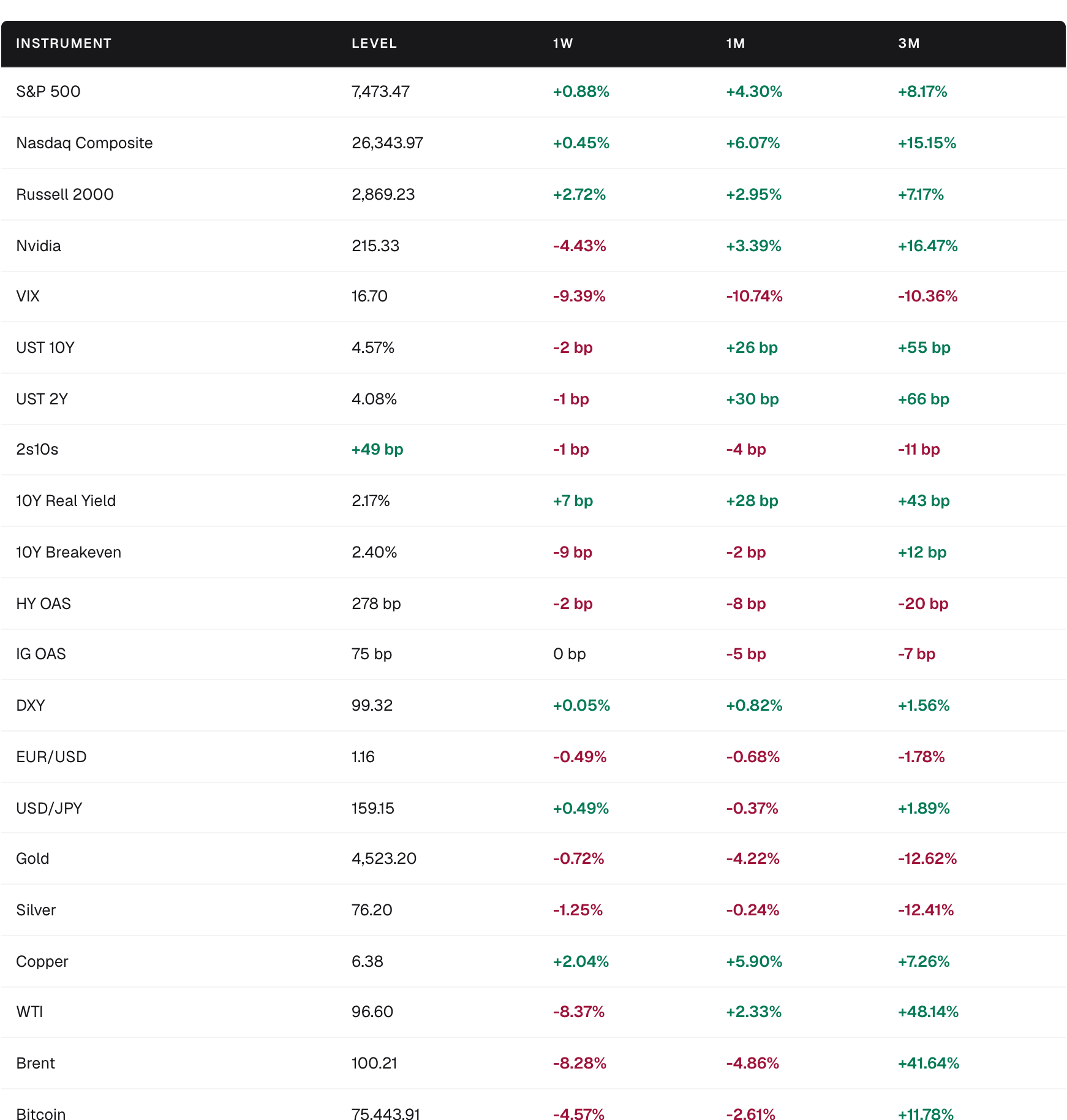

Risk assets held up despite a sharp crude reversal: the S&P 500 added +0.88% on the week to 7,473 (+4.30% 1M, +8.17% 3M), with the Russell 2000 leading at +2.72% as breadth broadened beneath the surface.

Energy was the dominant macro fulcrum: WTI fell 8.37% to $96.60 and Brent dropped 8.28% to $100.21 on the week, even as both remain up sharply over three months (+48.14% and +41.64%) on the lingering Iran/Strait of Hormuz overhang.

Rates were quietly constructive: UST10Y essentially unchanged at 4.57%, the 2s10s curve at +49 bps, while the 10Y real yield ticked up to 2.17% (+7 bps WoW). Credit refused to flinch, with HY OAS at 278 bps (-2 bps WoW) and IG OAS flat at 75 bps.

AI capex remained the equity engine into Nvidia earnings week; NVDA itself slipped 4.43% as positioning de-risked ahead of the print, but the Nasdaq still gained +0.45% and is +15.15% over three months.

Crosscurrents: gold fell 0.72% to $4,523 and bitcoin gave back 4.57% to $75,444, suggesting some rotation out of inflation/defensive hedges as the oil spike unwound and the dollar held near 99.3 on DXY.

Market Scorecard

Market Performance

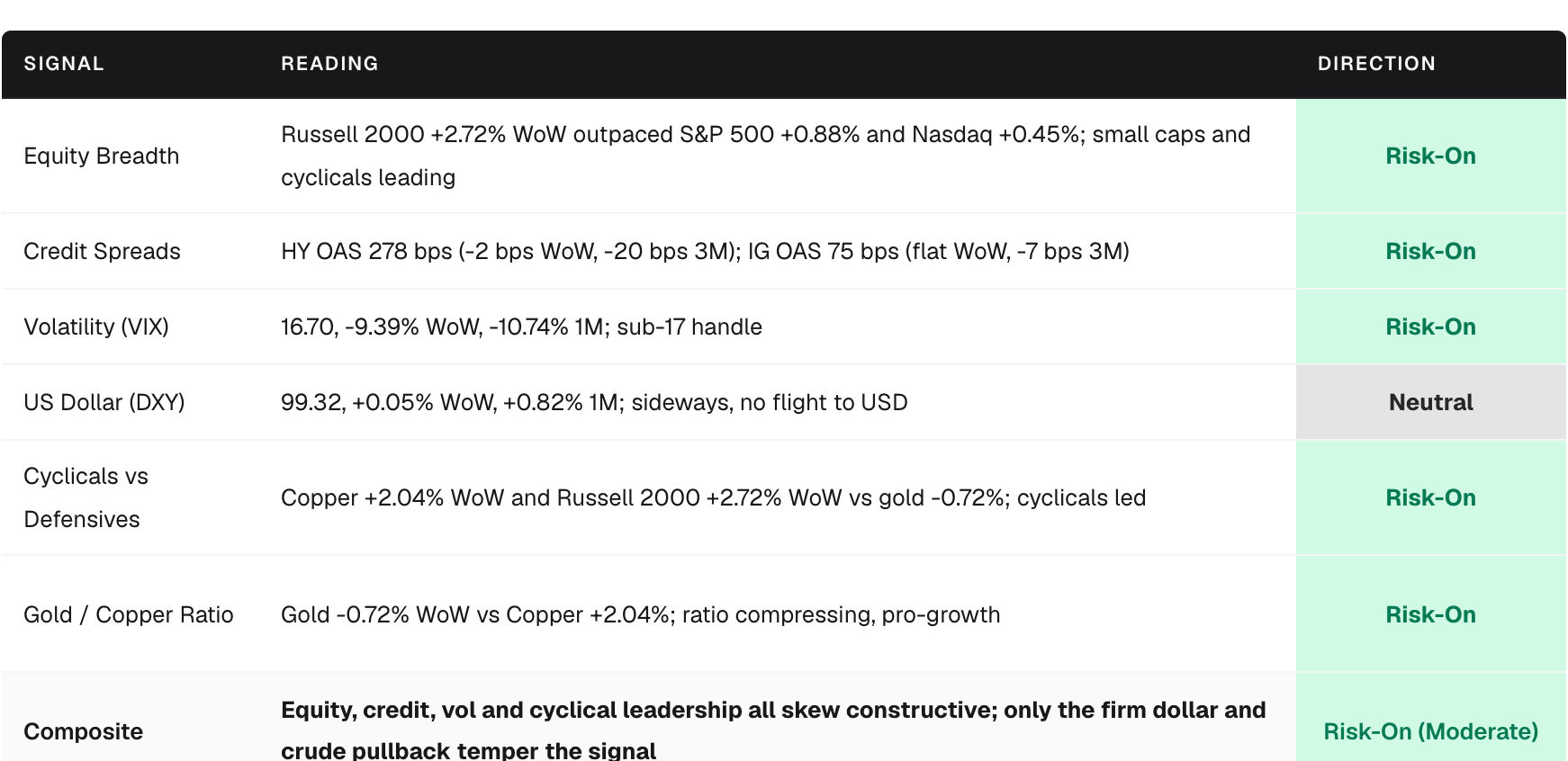

A mostly green week for risk, with the standout being the unwind in oil and the rotation into small caps and copper. Long-end yields barely moved despite the WTI plunge, suggesting the bond market is now anchoring more on growth and Fed patience than on the energy passthrough. Bitcoin and gold both softened, consistent with reduced demand for inflation/geopolitical hedges.

Key Drivers

Middle East oscillation: crude reversed sharply lower after the prior week’s spike, but May 21 commentary flagged renewed friction after Iran’s Supreme Leader stated enriched uranium “will not leave the country,” briefly pushing WTI back above $100 and yields higher intraday. The U.S. naval blockade of Iranian ports remained in place; S&P Global’s May Global Economic Outlook now assumes Brent above $100 through 2026 and cut 2026 global GDP to 2.2% from 2.9%.

Fed policy on hold: no FOMC event in the window, but the backdrop remained the April 28 to 29 hold at 3.50 to 3.75% on an 8-4 vote (the most dissents since 1992), with hawks worried about energy-driven inflation unanchoring expectations. Markets continue to price ~3.75% through Q2 with cuts pushed out.

AI capex super-cycle still intact: Big Tech ex-Nvidia generated $183.4B of operating cash flow in Q1 and spent $183.7B on capex and strategic investments. S&P 500 Q1 EPS tracking +27.7% YoY with an ~84% beat rate; 2026 EPS revised up to $333.25 (+21.3% YoY), Tech CY26 growth marked to +38.7%. Nvidia earnings landed mid-week as the marquee catalyst.

No top-tier macro prints in the week; focus turned to upcoming US core PCE (consensus +0.3 to 0.4% m/m), euro-area May flash inflation, Tokyo May core CPI, and Australia April CPI on the calendar for the following week.

IPO/AI signal: Cerebras (CRBS) priced May 14 at $5.5B (the largest US tech IPO of 2026 YTD) and closed day one near a $95B market cap, reinforcing investor appetite for AI infrastructure exposure into the week.

Sector and Thematic Notes

Winners

Small caps and cyclicals: Russell 2000 +2.72% WoW, Copper +5.90% 1M. Lower oil plus stable yields supported domestically-exposed names.

Industrials/Materials proxies: copper’s break higher and DAX-led European strength (+3.92% on the week per T. Rowe Price commentary) point to a cyclical bid on Middle East de-escalation hopes.

AI infrastructure ecosystem: capex confirmation from hyperscalers and Cerebras’s reception supported semis and AI-adjacent equipment names, even as NVDA itself sold off into earnings.

Losers

Energy: 8%+ drops in WTI and Brent pressured E&P and oilfield services after their multi-month rally.

Mega-cap AI hardware (NVDA -4.43%): de-risking into the print despite group-level enthusiasm; Nasdaq’s modest +0.45% vs Russell’s +2.72% shows the breadth shift away from megacaps.

Precious metals: gold -0.72% WoW, silver -1.25%, and the gold/copper ratio compressed as the geopolitical risk premium leaked out.

Crypto: BTC -4.57% on outflows per CoinShares; VanEck flagged Bitcoin hashrate down 13.2% from the November 2025 peak as US public miners pivot to AI/HPC hosting, a structural thematic crossover.

Risks to Watch

Oil round-trip risk: with Brent still +41.64% over three months and S&P Global modeling $100+ Brent through year-end, any renewed Iran/Hormuz flare-up could quickly re-tighten financial conditions through breakevens and the long end.

Inflation re-acceleration: 10Y breakevens at 2.40% look benign, but core PCE next week and the April CPI memory (+0.9% m/m headline on a 21.2% gasoline surge) keep the Fed hawkishly biased. Real yields at 2.17% are at cycle highs.

Nvidia/AI guidance disappointment: with Tech CY26 EPS growth marked to +38.7% and forward P/E at 22.2x, any softening in hyperscaler capex commentary would hit the largest contributors to S&P 500 earnings.

Dollar stickiness vs EM/European recovery: DXY +1.56% over three months despite a stable rates backdrop signals continued safe-haven bid; a sharper move higher would pressure commodities and EM credit.

Credit complacency: HY OAS at 278 bps is near cycle tights; any growth scare or default uptick from a sustained energy shock would widen aggressively from current levels.

Positioning Implications

Equity mix: the breadth shift into small caps and cyclicals, combined with HY at 278 bps and VIX at 16.7, argues for staying engaged in risk but rotating some megacap concentration into broader cyclicals and quality small caps; the Russell’s 1W lead over the Nasdaq is a notable signal to track.

Rates: with 10Y at 4.57% and real yields at 2.17%, the curve offers carry without much duration conviction. A barbell of front-end carry (UST2Y at 4.08%) plus selective belly exposure remains defensible until either oil rolls decisively or the Fed signals.

Credit: spreads leave little margin for error; consider up-in-quality within HY and using IG (75 bps) as a substitute for incremental beta rather than reaching down the stack.

Commodities: copper’s leadership over gold and oil’s pullback support a tilt toward industrial metals as the cyclical expression, while keeping a tactical hedge against an oil re-spike given the unresolved Iran standoff.

FX and alternatives: DXY’s range-bound action argues against directional dollar bets; in alternatives, the bitcoin pullback alongside miner pivots to AI hosting reinforces that the AI infrastructure theme is consuming capital across categories, a consideration for thematic sizing.

Cross Asset Performance Report