Release

End of Week Breakdown 08/05/2026

Overview

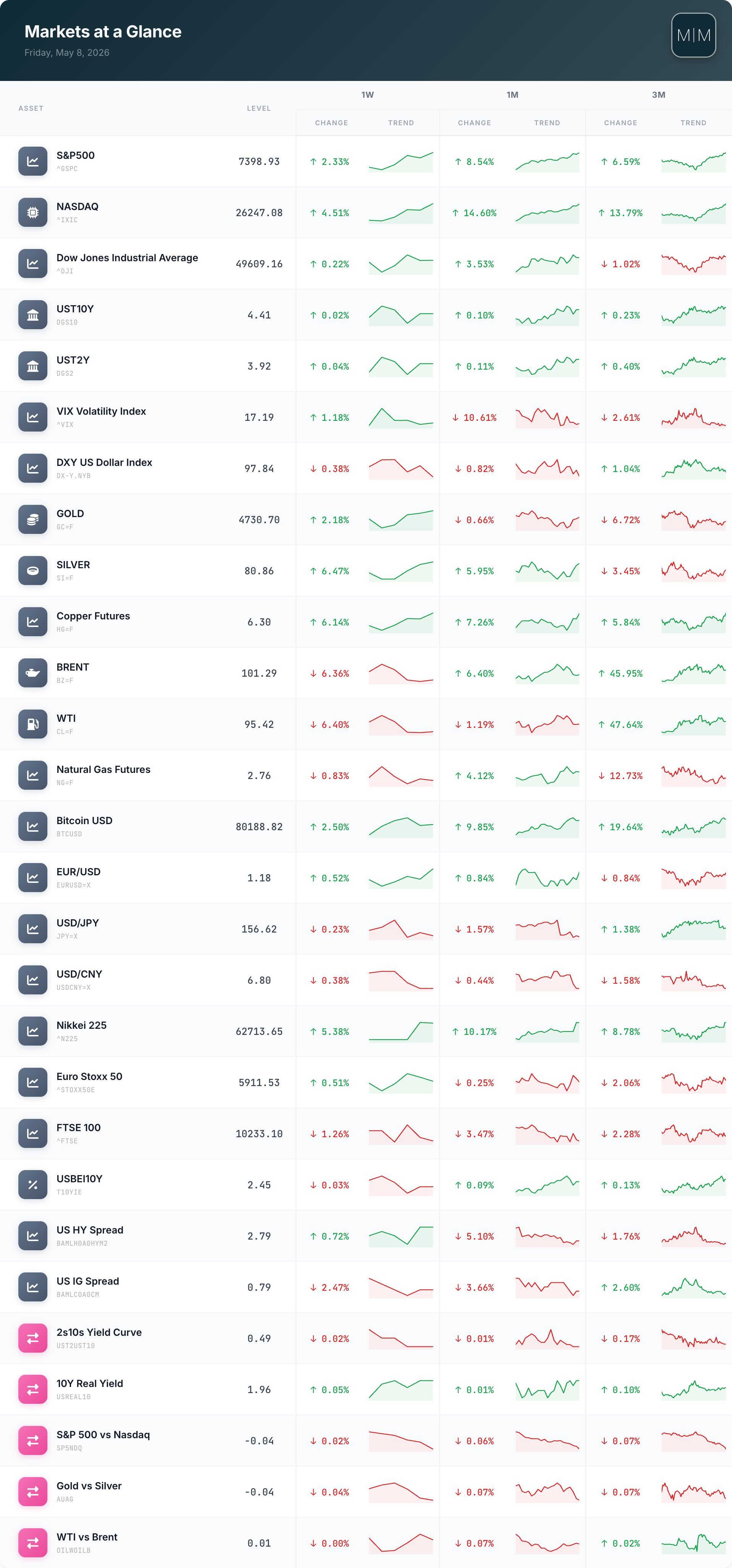

Oil reversed sharply. Brent fell 6.36% to $101.29 and WTI dropped 6.40% to $95.42, unwinding roughly half of the prior week’s spike as Hormuz de-escalation hopes built ahead of the May 14 to 15 Xi-Trump summit. The three-month gains remain enormous (Brent +45.95%, WTI +47.64%) but the immediate panic has bled out.

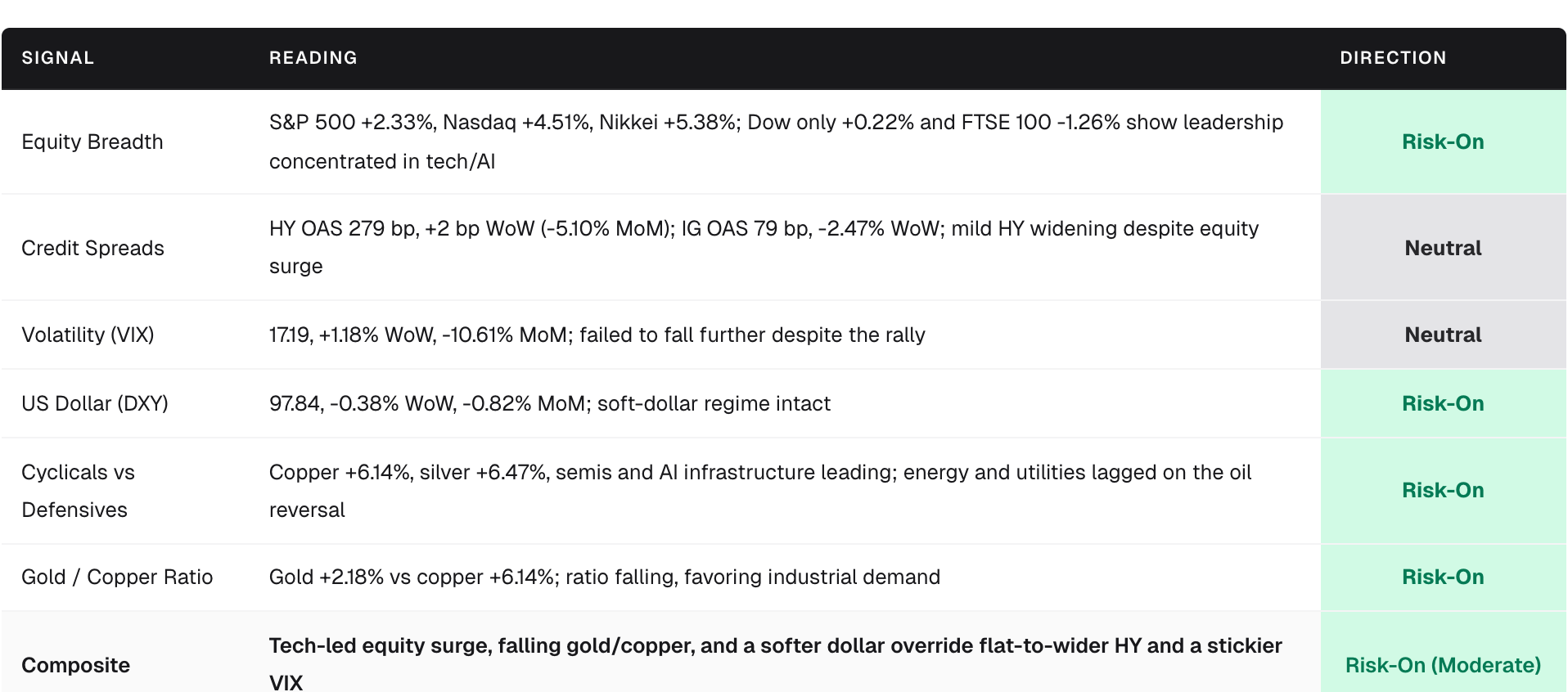

Equities ripped on the energy relief. S&P 500 +2.33% to 7,398.93, Nasdaq +4.51% to 26,247.08, Nikkei +5.38% to 62,713.65 on the back of a holiday-shortened tech-led rally and a Q1 earnings season tracking 27.7% blended YoY growth with 82% beats. The Dow lagged at +0.22%, underlining that this was a tech and AI capex tape, not a broad cyclical move.

Industrial metals joined the risk-on melt-up. Copper +6.14% on the week, silver +6.47%, gold +2.18% to $4,730 as the metals complex finally caught a bid after the prior month’s slide. Gold/copper falling reinforces the cyclical signal.

Credit and vol diverged. HY OAS widened modestly to 279 bp (+0.72% WoW) even as IG tightened to 79 bp (-2.47%); VIX ticked up to 17.19 (+1.18%) despite the equity rally. The cross-asset signal is constructive but no longer uniformly euphoric.

Norges Bank breaks ranks with a hike. A unanimous 25 bp move to 4.25% on May 6 is the only G10 actual policy change, while the Fed, ECB, BoE, and BoJ remain in their hawkish-hold posture and the ECB is now priced at roughly 90% for a June 11 hike.

Market Scorecard

Market Performance

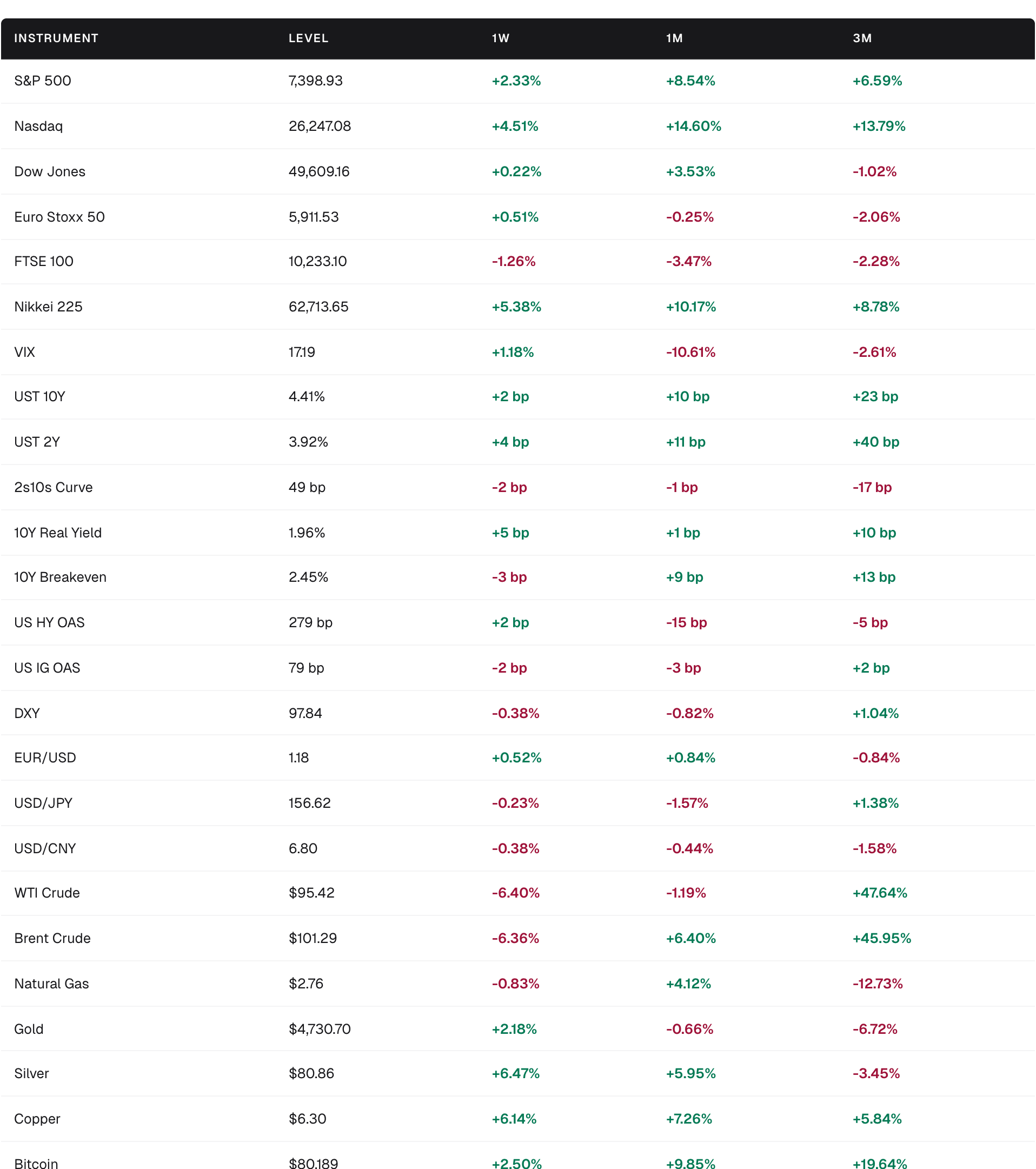

The defining move was a sharp reversal in crude that allowed equities and industrial metals to rally hard. Brent gave back 6.36% to $101.29 and WTI 6.40% to $95.42 as Strait of Hormuz tail risk faded into the upcoming Xi-Trump summit, even as the strait technically remains effectively closed. The Nasdaq added 4.51% to a fresh high at 26,247.08 on AI infrastructure demand and a strong earnings tape (Q1 S&P 500 blended growth tracking 27.7%, with 82% beats per FactSet). Japan was the standout developed market, with the Nikkei up 5.38% to 62,713.65 on tech and yen tailwinds, and Hong Kong (per T. Rowe Price) +2.39%. The FTSE 100 was the notable laggard at -1.26%, pressured by Trump tariff threats on the EU and UK-specific weakness. Gold reclaimed $4,730 (+2.18%), silver jumped 6.47% to $80.86, and copper added 6.14% to $6.30. The 10Y closed at 4.41%, essentially unchanged on the week, with the 2s10s curve at 49 bp. DXY softened to 97.84 and EUR/USD pushed to 1.18 on the ECB's hawkish lean. Bitcoin recovered 2.50% to $80,189.

Key Drivers

Oil reverses on de-escalation positioning. Brent’s 6.36% pullback came as markets priced in a constructive Xi-Trump summit on May 14 to 15, with China (a net oil importer working through 3 to 6 months of reserves) seen as having strong incentive to broker reopening of Hormuz. The strait remains effectively closed, however, leaving residual two-way risk into the meeting.

Q1 earnings sustained a double-digit surprise rate. S&P 500 blended growth at 27.7% and 82% beats (vs a 78% five-year average) extended the tech-led rally. AI infrastructure was the cleanest theme: Sterling Infrastructure +57%, AAON +49%, SiTime +48.62%, Akamai +41.62%, Western Digital +21.10%.

Norges Bank hikes 25 bp to 4.25%. Unanimous, citing inflation persistently above target. This is the first actual G10 rate increase in the current tightening reset, and a tangible validation of the broader hawkish lean.

ECB toward June 11 hike, ~90% priced. Lagarde’s “stands ready to adjust” language and Nagel’s open hint of a June move have hardened conviction since the prior week. The BoE is now described as moving closer to a hike this year, a meaningful shift from earlier “too quick” pushback from Bailey.

Fed: hawkish hold confirmed, hike pivot ruled out. Q1 GDP printed 2.0% annualized (vs 0.5% in Q4 2025). JPMorgan flags that despite the inflation noise, a shift to a renewed hiking cycle is unlikely. Powell has been characterised as “lame duck” with Warsh transition pending.

Tariff threats reintroduced. Trump’s renewed tariff threats against China and the EU pressured 10Y yields lower midweek and weighed on European indices, particularly the FTSE 100 (-1.26%).

Sector and Thematic Notes

Winners:

AI infrastructure and semis: Nasdaq +4.51%, with idiosyncratic 20% to 50% weekly gains in storage and AI-exposed mid-caps (WDC, SITM, AKAM). Earnings continue to validate the capex theme even as last week’s Meta/Microsoft scarring lingers.

Industrial metals: Copper +6.14%, silver +6.47%; gold/silver and gold/copper ratios falling. The metals complex has finally turned, consistent with the Hormuz de-escalation impulse and softer dollar.

Japan: Nikkei +5.38% in a shortened Golden Week schedule, hitting record highs on tech leadership and US-Iran diplomatic optimism, partly offsetting last week’s case to trim.

China and HK: CSI 300 +1.34%, Hang Seng +2.39% on resilient domestic demand and pre-summit trade optimism, a notable improvement from the prior week’s lag.

Losers:

Energy equities and crude longs: WTI -6.40%, Brent -6.36%; energy sector lagged the S&P advance, validating last week’s case to trim into strength.

FTSE 100, -1.26%: caught between tariff threats, rising BoE hike risk, and weak commodity beta after the oil reversal.

Natural gas, -0.83% on the week, -12.73% on three months: continues to underperform the broader energy reset.

HY credit: OAS widened 2 bp to 279 bp despite equities at highs, the only modest cross-asset blemish

Risks to Watch

1. Xi-Trump summit binary, May 14 to 15. With Brent's pullback already pricing partial de-escalation, a failure to deliver on Hormuz reopening or new tariff escalations could send crude back through $110 and reverse this week's risk-on tape rapidly.

2. April US CPI on the calendar. Consensus headline 3.4% YoY with 0.4% core MoM. After the oil shock and with breakevens at 2.45%, an upside surprise would test the JPMorgan thesis that a Fed re-hike is off the table.

3. ECB June 11 hike: priced but not delivered. With ~90% probability embedded, any signal of a delay would whipsaw EUR/USD (1.18) and European banks; a confirmed hike, while expected, would push 2Y front ends globally.

4. Tariff escalation. Renewed Trump threats against the EU and China have already moved long yields and FTSE; a concrete tariff announcement before or after the summit is a clear left-tail for cyclicals and EU equities.

5. Norges Bank as canary. A unanimous hike is a reminder that small-economy central banks are willing to lead. Watch the Riksbank, RBA, and BoC for follow-through, which would tighten the global liquidity impulse faster than US-only models suggest.

Positioning Implications

The “trim energy into strength” call is now playing out. Brent -6.36% validates the prior week’s view; residual exposure is cleanest via diversified energy equities or oil-levered credit rather than spot crude into the binary summit.

AI infrastructure dispersion remains the trade. Nasdaq +4.51% with idiosyncratic 20% to 50% earnings movers reinforces that pair trades and selective AI capex beneficiaries (semis, networking, storage) are working better than directional Nasdaq beta with VIX still at 17.19.

Industrial metals deserve a fresh look. Copper and silver have decisively turned with the dollar soft and global PMIs holding up. The gold/copper ratio is in the early stages of rolling over; relative-value over outright gold is the cleaner expression.

Credit asymmetry warrants downshifting HY beta. HY at 279 bp widened on a +2.33% S&P week, the first hint that credit is no longer leading the rally. IG at 79 bp is tight but better placed if the equity tape stalls.

Duration: front-end shorts still cleanest. UST 2Y +40 bp on three months and a unanimous Norges hike argue against adding duration. The 10Y at 4.41% looks range-bound until April CPI clears or the summit delivers a surprise.

Europe: trim the underweight further. Euro Stoxx 50 +0.51% with an ECB hike all but priced and EUR/USD firming favors European banks and value over growth, but UK exposure is now harder to defend with the FTSE -1.26% and tariff risk live.

Japan: re-engage selectively. Nikkei +5.38% and yen at 156.62 partially reverse last week’s case to trim, but BoJ “hawkish inclinations” mean exporter exposure should be paired with FX hedges or domestic-demand longs.

Crypto: the spot-flow disconnect resolved upward. BTC +2.50% to $80,189 with three-month gains of 19.64% suggests last review’s flow buildup is being released. Position sizing remains the discipline given the still-elevated correlation to risk sentiment.

Cross Asset Performance Report