Standoff

End of Week Breakdown 03/05/2026

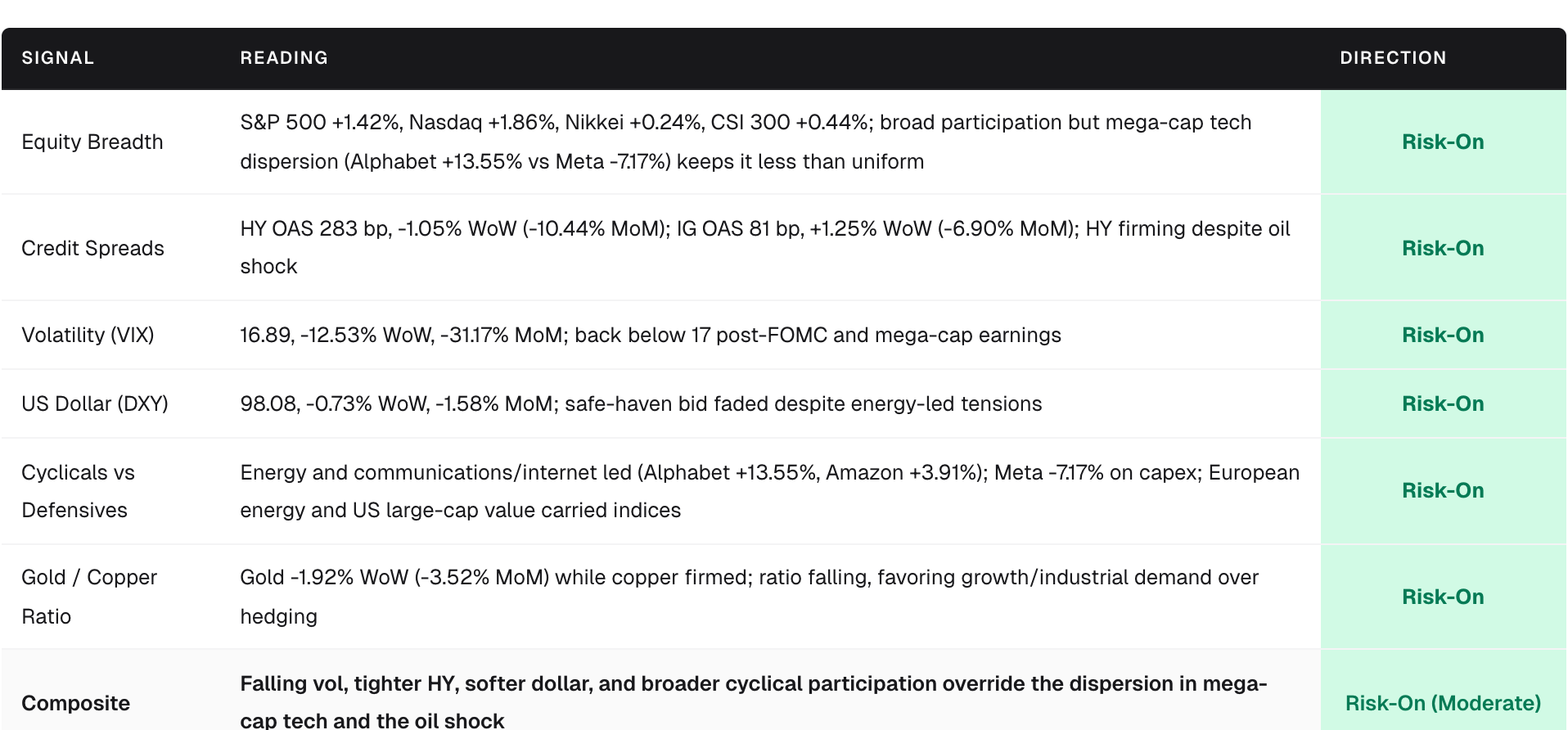

Overview

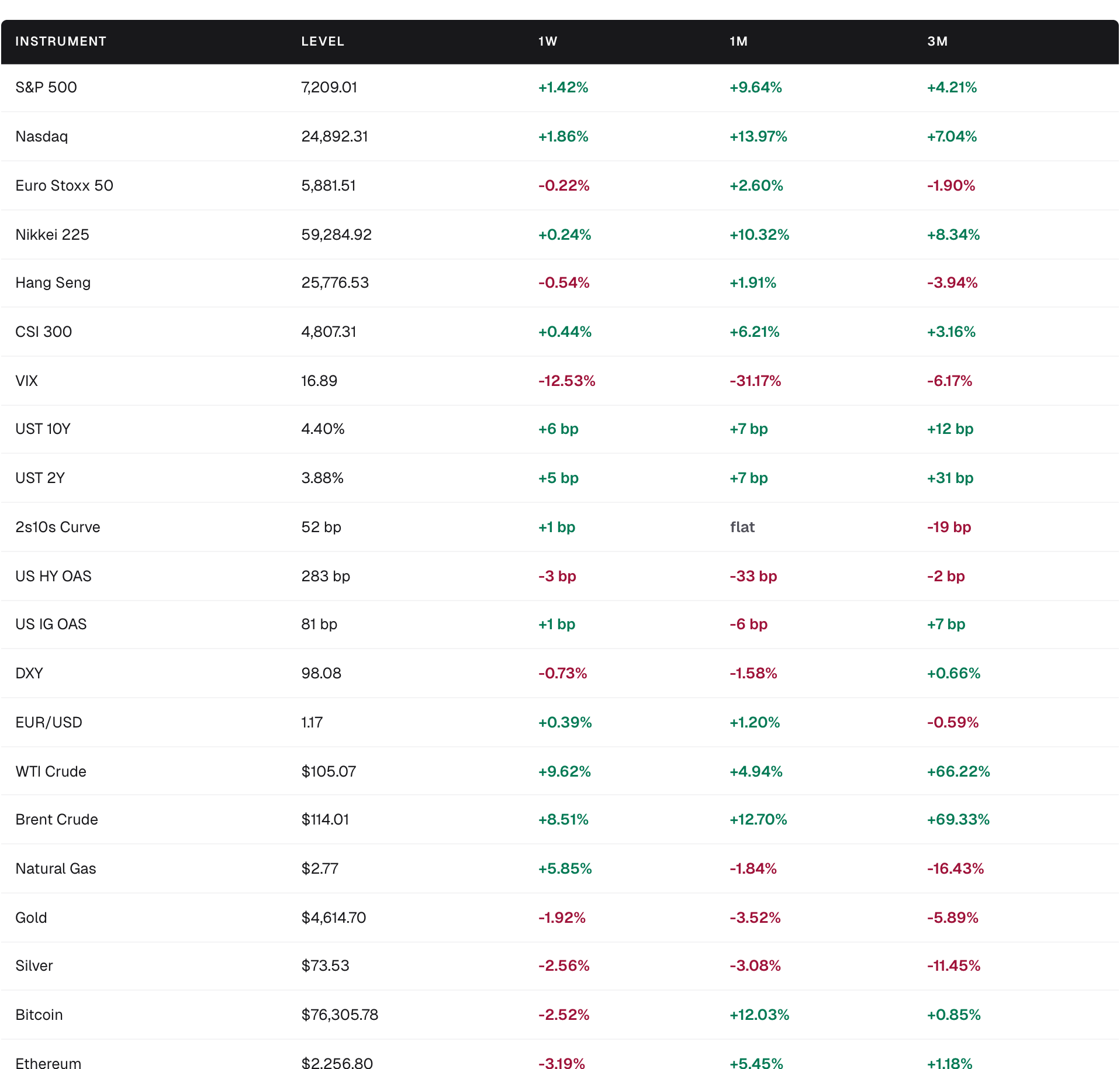

Oil broke through $100 and kept going. Brent surged another 8.51% on the week to $114.01 and WTI gained 9.62% to $105.07, extending a three-month rally of roughly 67% to 69% as Hormuz disruption fears persisted and Trump warned of potential strikes on Iranian infrastructure. Brent is now up 12.70% on the month.

Risk assets shrugged off the energy shock. The S&P 500 added 1.42% to 7,209 and the Nasdaq rose 1.86% to 24,892, with VIX collapsing 12.53% to 16.89. The post-FOMC and mega-cap earnings reaction was constructive on aggregate, even as individual names diverged sharply.

Mega-cap tech bifurcated. Alphabet ripped 13.55% on standout AWS-style cloud growth, Amazon climbed 3.91%, but Meta fell 7.17% and Microsoft slipped 1.92% as capex-to-revenue concerns surfaced. The dispersion is the story, not the index print.

Central banks held, but the bias shifted hawkish. The Fed left 3.50% to 3.75% unchanged on an unusually split 8-4 vote with one cut dissent; the ECB tilted toward a likely June hike; the BoE saw a hawkish dissent; markets now price no Fed cuts in 2026 and possible 2027 hikes.

Credit and the dollar diverged from the oil shock. HY OAS tightened to 283 bp (-1.05% WoW), DXY softened 0.73% to 98.08, and the 10Y yield was effectively unchanged at 4.40%. The bond market is, for now, treating the energy spike as a relative-price event rather than a sustained inflation regime change.

Market Scorecard

Market Performance

US equities led developed markets higher, with the Nasdaq's 1.86% weekly gain pushing its monthly tally to 13.97% despite a brutal Meta print. Europe was effectively flat (Euro Stoxx 50 -0.22%), recovering composure after the prior week's energy-driven drawdown. Asian indices were mixed, with the CSI 300 nudging up 0.44% and Nikkei effectively flat at +0.24% as the BoJ's 6-3 split and stronger yen weighed on exporters. The defining macro print remains energy: Brent breached $100 and accelerated to $114.01, WTI to $105.07, and natural gas firmed 5.85%. Treasury yields barely moved at the long end (10Y +0.06% to 4.40%) but credit notably firmed, with HY OAS down to 283 bp. Precious metals continued to lose ground, gold off 1.92% to $4,614 and silver -2.56%, while bitcoin slipped 2.52% to $76,306.

Key Drivers

Brent through $100, WTI through $105. The Hormuz risk premium that drove last week’s spike compounded as Trump warned of possible US action against Iranian infrastructure. Brent’s three-month gain of 69.33% is now the dominant macro signal, though credit and the dollar are not yet trading it as a regime change.

Fed: hawkish hold. Rates left at 3.50% to 3.75% on an 8-4 vote, the deepest split since 1992, with Miran dissenting for a cut and others pushing back on easing language. Markets now price no 2026 cuts and possible 2027 hikes. Powell will reportedly stay on as governor after Warsh assumes the chair in mid-May, an institutional change worth tracking.

ECB pivots toward a June hike. Lagarde flagged a move from baseline; sources signal a June hike is the working assumption, with two hikes embedded in baseline forecasts. This is a meaningful reversal of the prior “extended pause” framing.

BoE and BoJ also tilt hawkish. BoE held at 3.75% with one hike dissent (Pill); BoJ held at 0.75% on a 6-3 split, the widest under Ueda, with core inflation projected above 2% into 2028 and yen strengthening post-decision.

Mega-cap earnings: dispersion, not direction. Alphabet was the clear winner (+13.55% on the week) on accelerating cloud and AI monetization. Amazon delivered its best AWS growth since COVID (+3.91%). Microsoft (-1.92%) and especially Meta (-7.17%) were punished as capex outpaced revenue and 2027 margin guides disappointed. Apple still pending.

Credit firms in the face of the oil shock. HY OAS at 283 bp tightened a further bp despite Brent at $114; equity vol collapsed to 16.89. The cross-asset signal: markets are interpreting the energy move as bounded and supply-driven rather than demand-destructive.

Sector and Thematic Notes

Winners:

Energy and oil-levered names: Brent +8.51%, WTI +9.62%; the move continues to drive index-level rotation into US energy and selective European producers.

Cloud and search/internet: Alphabet +13.55% on a multi-quarter cloud acceleration and AI monetization, the standout megacap; Amazon +3.91% on AWS reacceleration.

European banks/value: flat Euro Stoxx 50 masks rotation into oil-levered and rate-sensitive names as the ECB tilts hawkish.

Crypto factors: Bitcoin spot ETFs took $1.9 billion of recent inflows including $630 million on May 1; Ether ETFs $101 million on May 1, even as spot BTC slipped 2.52%.

Losers:

Meta, -7.17%: capex outpacing revenue, weaker 2027 profitability guide; the cleanest example of “good is not good enough” in mega-cap tech.

Microsoft, -1.92%: Azure +40% YoY was strong, but rising capex weighed on the print relative to peers.

Precious metals: gold -1.92%, silver -2.56%, with three-month declines of 5.89% and 11.45% respectively. Despite a softer dollar, the trade is not finding traction.

Bitcoin and Ether: down 2.52% and 3.19% on the week; ETF inflows have not arrested the spot drift in the upper-$70k range.

Hang Seng: -0.54% WoW, -3.94% 3M; remains the global laggard.

Risks to Watch

1. Iran/Venezuela escalation tail. Brent at $114 already reflects significant premium; an actual strike on Iranian infrastructure or a Hormuz closure event would push prices materially higher and likely break the cross-asset complacency now visible in HY and VIX.

2. Hawkish central bank repricing. The Fed's 8-4 split, ECB June hike signaling, and BoE/BoJ dissent collectively represent a meaningful reversal of the holding-pattern narrative. If front-end yields catch up to the rhetoric (UST 2Y is up 31 bp on three months), risk assets could face a delayed rates shock.

3. Mega-cap tech capex digestion. Meta's 7.17% drawdown and Microsoft's softness highlight that AI capex is increasingly priced as a margin headwind, not a growth call. Apple's pending result and forward guidance from the cohort will set the tone for whether the Nasdaq's 13.97% monthly gain is durable.

4. Macro data backlog. With Q1 GDP advance, March PCE, ISM manufacturing, Eurozone flash CPI, and China PMIs all due imminently, a hot inflation print on top of the oil shock would force a sharper hawkish recalibration.

5. BoJ-driven yen strength. A 6-3 split with core inflation projected above 2% into 2028 raises the probability of a near-term hike. A meaningful USD/JPY retracement from the 158 area would pressure the Nikkei carry trade and Japanese exporters.

Positioning Implications

Energy: trim into strength. WTI +66% and Brent +69% over three months mean positioning is crowded and the risk/reward is increasingly asymmetric. Expressing the residual view through diversified energy equities or oil-levered credit, rather than outright crude, may better balance the binary diplomatic risk.

Mega-cap tech: lean into dispersion, not the index. Alphabet’s earnings response separates it from the cohort; Meta and Microsoft’s reactions show that beta to the AI capex theme is no longer one-directional. Pair trades within the basket are arguably more attractive than directional Nasdaq exposure with VIX at 16.89.

Duration: the case for adding has weakened. With the Fed hawkish-held, the ECB pivoting to a hike, and the BoJ tilting more split, the prior bias to add duration on weakness is harder to defend. Front-end shorts remain the cleanest expression of the central bank message; long-end yields have notably failed to rise with oil.

Credit: HY at 283 bp leaves no margin. Tightening into an oil shock is unusual and probably unsustainable if energy remains above $110. Reducing HY beta and rotating toward IG (81 bp, modestly wider WoW) is worth considering, though IG is hardly cheap either.

Europe: the underweight bias loosens. Euro Stoxx 50 nearly flat despite Brent breaching $114 suggests resilience; an ECB hike cycle could support European banks. Selective long exposure is more defensible than at last review.

Japan: trim conviction. Nikkei flat on the week with a hawkish-tilting BoJ and stronger yen risk argues for trimming the structural overweight that worked through Q1.

Precious metals: still no entry signal. Gold’s continued slide alongside a softer dollar is a notable divergence and suggests positioning rather than macro is driving the move. Wait for stabilization before adding.

Crypto: ETF flows vs spot disconnect. $1.9 billion into BTC ETFs has not lifted price; this divergence usually resolves in one direction sharply. Maintaining position size discipline is more important than directional conviction here.

Cross Asset Performance Report