Staying Strong

Multi Asset Report 4

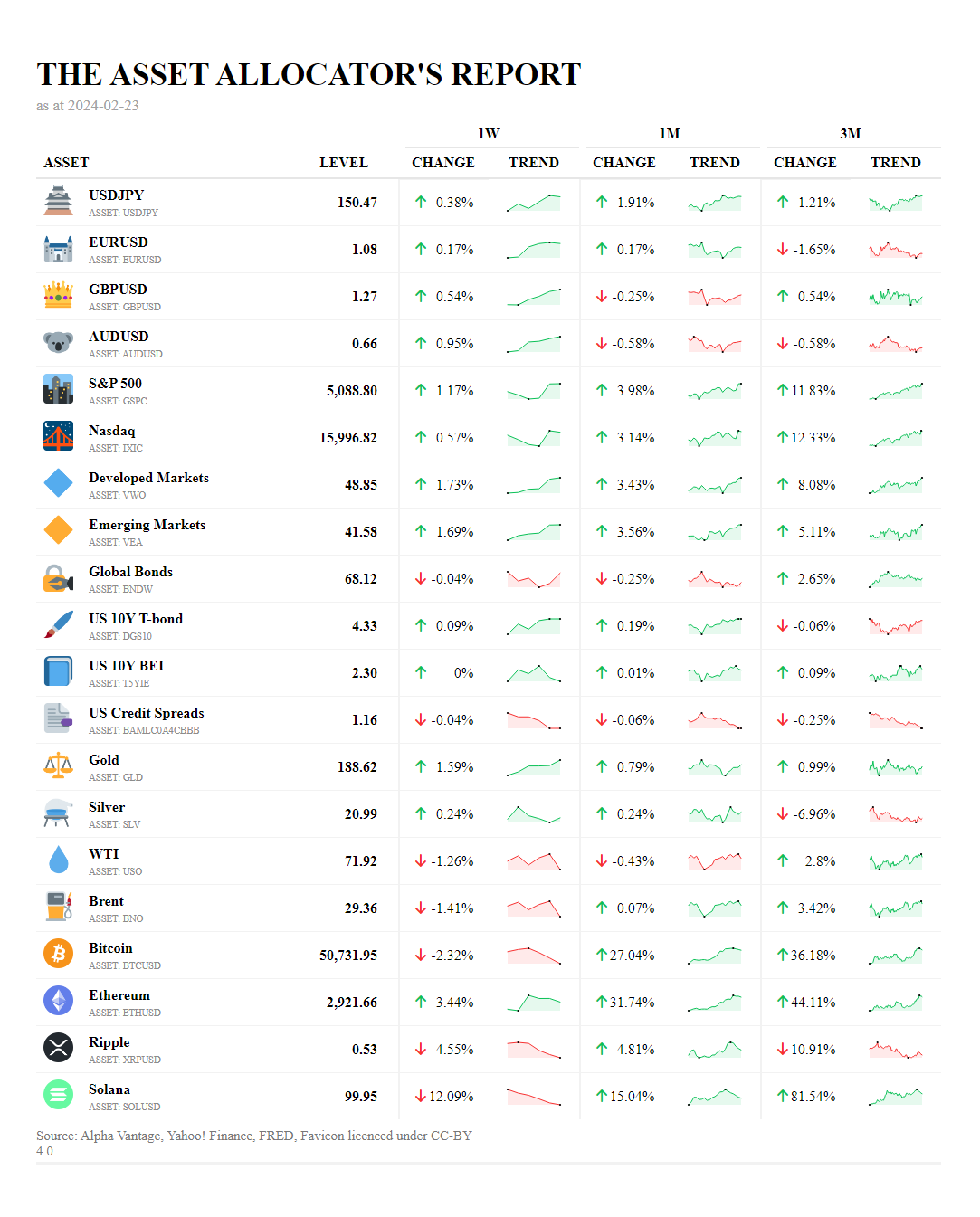

We observe a dynamic and robust equities market that reflects both the opportunities and challenges present in the current global economic landscape. The S&P 500 has shown a remarkable 1-week increase of 1.17%, a 1-month increase of 3.98%, and an impressive 3-month growth of 11.83%. This performance is indicative of a resilient U.S. equities market that continues to attract investment despite broader economic headwinds.

The technology-heavy Nasdaq index also demonstrates strong performance with a 0.57% increase over the past week, a 3.14% increase over the past month, and a significant 12.33% increase over the past three months. This suggests that technology stocks remain a driving force in the market, likely buoyed by recent earnings reports from industry leaders such as Nvidia, which has shown exceptional revenue growth driven by demand for AI chips.

In the commodities sector, Gold has seen a steady increase, with a 1.59% rise over the past week, aligning with its status as a safe-haven asset amidst geopolitical tensions and economic uncertainty. The oil markets, however, have faced downward pressure, with WTI and Brent crude experiencing declines of 1.26% and 1.41% respectively over the past week, reflecting the complex interplay of supply dynamics and geopolitical factors influencing the energy sector.

Cryptocurrencies have shown mixed results, with Bitcoin experiencing a 2.32% decrease over the past week but maintaining a robust 27.04% and 36.18% increase over the past month and three months, respectively. Ethereum has followed a similar pattern, suggesting a continued investor interest in digital assets as a component of diversified portfolios.

In the context of global events, the performance of equities and commodities must be viewed through the lens of ongoing geopolitical tensions, particularly the economic ramifications of the conflict in Ukraine and the strategic maneuvers by Russia and China. Additionally, the Federal Reserve's stance on inflation and interest rates continues to be a critical factor for investors, as evidenced by the cautious optimism in the bond markets and the nuanced reactions to potential Fed policy shifts.

"The investor's chief problem—and even his worst enemy—is likely to be himself." - Benjamin Graham

Upgrade to premium to get access to the high resolution pdf report download link below and exclusive insights and research