Waiting

Intraweek Breakdown 29/04/2026

Overview

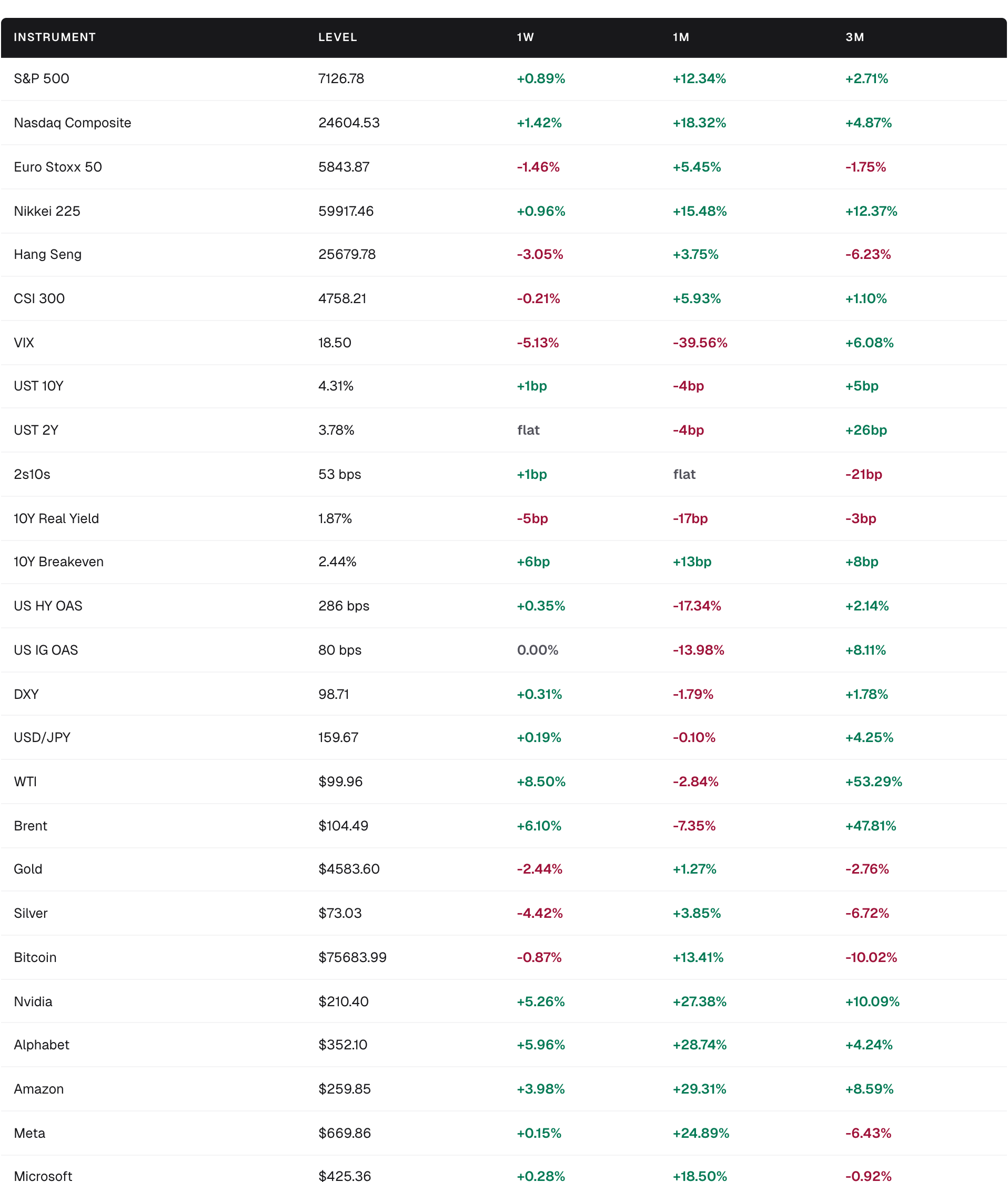

Risk assets held near records but momentum cooled into a heavy central bank and earnings week: S&P 500 at 7,126.78 (+0.89% 1W, +12.34% 1M), Nasdaq at 24,604.53 (+1.42% 1W, +18.32% 1M), with the VIX compressed to 18.50 (-5.13% 1W, -39.56% 1M).

Geopolitics is the dominant friction: stalled US-Iran talks and an ongoing Hormuz blockade pushed WTI to $99.96 (+8.50% 1W, +53.29% 3M) and Brent to $104.49 (+6.10% 1W, +47.81% 3M), squeezing European equities (Euro Stoxx 50 -1.46% 1W) even as US tech kept rallying.

BoJ held at 0.75% (6-3) on April 28 and halved its growth forecast; Fed (April 30), BoC, ECB and BoE are expected to hold, with markets now pricing the first Fed cut only in December 2026.

Credit remains a green light: HY OAS at 286 bps and IG OAS at 80 bps, both essentially flat on the week but tighter by 17.3% and 14.0% on the month respectively, signalling no funding stress despite the oil shock.

Precious metals corrected (gold $4,583.60, -2.44% 1W; silver -4.42% 1W) as the dollar firmed (DXY 98.71, +0.31% 1W) into the Fed; Bitcoin slipped to $75,684 (-0.87% 1W) but is still +13.41% on the month.

Market Performance

US indices and AI mega-caps remain the engine of returns, with the Nasdaq +18.3% on the month and Alphabet, Amazon, Meta and Nvidia all up 24-29% over 30 days. Energy is the standout macro story: WTI and Brent are up roughly 50% over three months on Hormuz disruption. Europe and Hong Kong lagged on the same oil shock, while Japan held up on AI/SoftBank-led demand. Rates barely moved, with the 10Y at 4.31% and 2s10s at 53 bps, even as the BoJ held and the Fed prepared to.

Key Drivers

BoJ on hold at 0.75% (April 28, 6-3 vote): inflation seen “significantly” higher, but growth forecast halved, leaving USD/JPY pinned at 159.67.

Fed window opening April 30: consensus is a hold at 3.50-3.75%, with markets now expecting the first cut only in December 2026. Powell’s final meeting before stepping down May 15 raises communication risk.

Hormuz/Iran: US-Iran talks collapsed, blockade halving Saudi exports per Bloomberg shipping data; oil’s +8.5% weekly move in WTI is the cleanest risk transmission and a direct headwind to European cyclicals and UK retail.

Earnings superweek: Microsoft, Alphabet, Amazon, Meta and Apple report against ~$15T combined market cap; Q1 S&P earnings tracking 84% positive EPS surprises so far on 28% reported. Mega-cap 1M moves (GOOGL +28.7%, AMZN +29.3%, META +24.9%) leave little room for guidance disappointment.

Macro data ahead, not behind: US Q1 GDP (consensus 2.1% vs Q4 0.5%) and March core PCE (0.3% MoM) print April 30; Eurozone Q1 GDP and country CPI flashes Thursday.

Crypto policy: CLARITY Act discussion at the Bitcoin Conference April 28 framed as a potential structural unlock for bank custody, stablecoins and tokenization; no immediate price translation, with BTC -0.87% on the week.

Risks to Watch

Fed communication risk April 30: any signal that the cutting bar is rising could reprice the +18% 1M Nasdaq move and tighten financial conditions via the dollar.

Hormuz escalation: a sustained Brent print above $110 would feed back into breakevens (already 2.44%, +13bp 1M) and threaten the disinflation narrative central banks are leaning on.

Mega-cap earnings disappointment: with MSFT, GOOGL, AMZN, META reporting after 25-29% 1M rallies, capex and AI monetization commentary carry asymmetric downside.

Complacent volatility: VIX at 18.5 and -39.6% 1M leaves little cushion against an oil, Fed or earnings surprise.

EU/UK growth drag: oil-driven hit to consumption (UK retail already softening) into ECB and BoE meetings risks a hawkish-hold-into-weakening-growth setup.